021-50368000

021-50368000

Import Trade Statistics

The total value of Chinas import and export in September 2023 was US $520.55 billion, up 3.8% compared with August this year and down 6.2% compared with September last year; In terms of exports, the export value in September was 299.13 billion US dollars, an increase of 5.0% compared with August this year, and a year-on-year decrease of 6.2% compared with September last year; In terms of imports, the value of imports in September was US $221.42 billion, up 2.3% from August this year and down 6.2% from September last year. The trade surplus in goods was US $77.71 billion, representing a total of US $630.3 billion from January to September.

In September 2023, Chinas import of mechanical and electrical products was 6180.7 billion yuan (export 1287.69 billion yuan), and the cumulative import of mechanical and electrical products from January to September was 47,018.1 billion yuan (export 10255.06 billion yuan), a year-on-year decrease of 9.0 % (export increase of 3.3 percent) compared with last year; Among them, the import of integrated circuit in September was 425.5 billion (export 24.33 billion), worth 233.1.6 billion (export 97.14 billion) yuan, and the import from January to September was 17,668.2 billion (export 688.37 billion) yuan, 14.4 % lower than last year (export decreased 8.3 %). In September, the import of medical devices was 87.3 billion yuan (export 12.66 billion yuan), and the import from January to September was 729.3 billion yuan (export 95.44 billion yuan), with a year-on-year increase of 1.7 percent (export increase of 2.6 percent).

1.Announcement No. 127 of the General Administration of Customs of 2023 (Announcement on dealing with Matters related to Violations of Active Disclosure)

Issuance Date: 2023-10-08

Effective Date:2023-10-11

To further optimize the business environment, promote the development of Chinas high quality, according to the law of the Peoples Republic of China customs law of the Peoples Republic of China on administrative punishment law of the Peoples Republic of China customs inspection regulations and the provisions of the relevant laws and regulations, The relevant matters concerning the handling of acts of import and export enterprises and units that voluntarily disclose violations of customs regulations before customs detection and correct them in time are hereby announced as follows:

I. Import and export enterprises and units that voluntarily disclose acts in violation of Customs regulations shall not be subject to administrative punishment under any of the following circumstances:

(1) voluntarily disclosing to the Customs within six months from the date of the occurrence of the tax-related violation.

(2) voluntarily disclosing to the Customs within six months but within two years from the date of the tax-related violation, the omission or underpayment of taxes accounts for less than 30% of the tax payable, or the omission or underpayment of taxes is less than RMB 1 million yuan.

(3) Affecting the administration of export tax rebate by the State:1. Voluntarily disclose to the customs within six months from the date of the violation;2. Actively disclose to the customs within six months but within two years from the date of the violation, which affects the administration of export tax rebate of the state and may be refunded less than 30% of the tax repayable, or may be refunded less than RMB 1 million.

(4) the actual unit consumption of a processing trade enterprise is lower than the declared consumption due to reasons such as process improvement or inaccurate declaration of the proportion of non-bonded materials and parts used, and the remaining materials and parts, semi-finished products and finished products resulting therefrom have not been disposed of, or have been exported again through processing trade.

(5) where the provisions of Item (1) of Article 15 of the Regulations on the Implementation of Customs Administrative Penalties of the Peoples Republic of China are applied and the rectification is made in a timely manner without causing harmful consequences:

1. Actively disclose to the customs before 24:00 on the last day of the month when the violation occurs and affect the statistics of the total value of RMB 10 million or less;

2. The violation is voluntarily disclosed to the customs within 3 natural months after 24:00 on the last day of the month and affects the total value of RMB 5 million or less.

(6) it shall be dealt with in accordance with Item (2) of Article 15 of the Regulations on the Implementation of Customs Administrative Penalties of the Peoples Republic of China.

(7) Acts in violation of Customs regulations that are subject to the provisions of Article 18 of the Regulations of the Peoples Republic of China on the Implementation of Customs Administrative Penalties, which do not affect the states administration of prohibitions on entry and exit, administration of export tax rebates, tax collection and administration of licenses.

(8) Acts of import and export enterprises and units in violation of the regulations on Customs inspection and quarantine business, and they can go through the customs formalities in a timely manner without causing harmful consequences (see Appendix 1). With the exception of those related to quarantine matters and those related to safety, environmental protection and health matters in inspection.

II. Import and export enterprises and units shall voluntarily report their tax-related violations to the Customs in writing and correct them in a timely manner. If the Customs determines that the disclosure is voluntary, the import and export enterprises and units may apply to the Customs for reduction or exemption of overdue tax fees according to law. In case of compliance with relevant regulations, the Customs will grant a reduction or exemption.

III. The behavior of an import or export enterprise or unit that voluntarily discloses and is subject to a warning or a fine of less than RMB 1 million by the Customs shall not be included in the record of the credit status of the enterprise determined by the Customs. If an enterprise with advanced certification actively discloses the behavior in violation of customs regulations, the customs shall not suspend the application of corresponding management measures to the enterprise during the investigation. However, the inspection related to safety, environmental protection and health matters are excluded.

IV. The relevant provisions of this announcement shall not apply to the same violation of customs regulations (refers to the same nature and violation of the same provisions of the same law) voluntarily disclosed to the Customs for the second time or more within one year (12 consecutive months) by the import and export enterprises and units.The relevant provisions of this announcement shall not apply to the import and export enterprises or units that voluntarily disclose to the customs once or more rights licenses of the authorized person based on the same goods by the right holder.

V. If an import or export enterprise or unit makes disclosure to the customs on its own initiative, it shall fill in the Report Form of Active Disclosure (see Appendix 2), attach account books, documents and other materials, and report to the customs at the place of declaration, the place of actual import or export or the place of registration.

This announcement shall be valid from October 11, 2023 to October 10, 2025. Notice No. 54 of 2022 of the General Administration of Customs shall be abrogated at the same time.

LINK

http://www.customs.gov.cn/customs/302249/2480148/5417968/index.html

Policy Interpretation

Change point 1: The scope of application of proactive disclosure has been expandedThe latest announcement, 127, explicitly contains: The initiative disclosure of preferential policies affecting customs tax collection, national tax rebate management, processing trade supervision, customs statistical accuracy or supervision order, and some violations related to inspection matters (compared with the original 2022 GGA54 announcement, the scope of application is only "tax-related violations", the scope is expanded).

This new announcement will include the relevant scope, for the majority of import and export enterprises in the actual problem of such violations, can apply the requirements of the announcement to the customs for active disclosure, enjoy preferential policies, eliminate the potential risks of the company.

Change point 2: the time limit and times of partial application are relaxed1) For the voluntary disclosure of preferential treatment measures for violations involving customs tax collection or export tax rebate occurring for more than 6 months, the revised time is "more than six months but within two years from the date of occurrence of tax-related violations" (relaxed compared with within one year as stipulated in the original Announcement No. 54 of the General Administration of China in 2022).2) The relevant provisions of this announcement shall not apply to those who voluntarily disclose the same tax-related violation to the customs again "to" the relevant provisions of this announcement shall not apply to those who voluntarily disclose the same violation to the Customs for the second time or more within one year."

In general, the new announcement for the active disclosure of import and export enterprises, compared with the original announcement in the scope and disposal measures more relaxed, greatly conducive to business owners to the customs to actively disclose management violations or tax-related violations, to solve risks and hidden dangers.

2.Announcement No. 131 of the General Administration of Customs in 2023 (Announcement on the Decision on the Classification of "Heat-Conducting Liquid" commodities)

Issuance Date: 2023-10-11

Effective Date:2023-10-11

For the import and export of goods to the consignee or consignor and the agent right to declare product classification, guarantee the unity of the customs commodity classification, according to the law of the Peoples Republic of China on import and export goods customs commodity classification management stipulation "the relevant provisions of the (order no. 252 published of the General Administration of Customs). The General Administration of Customs has translated the opinions of the WCO Coordination System Committee on the classification of "heat-conducting liquids" commodities into the decision on the classification of commodities (see the appendix), and hereby publishes it. The original decision on commodity classification of "Mixture of benzyltoluene and phenyl ethane" (Decision No. Z2010-0006, Announcement No. 15, 2010 issued by the General Administration of Customs) will become invalid at the same time.

LINK

http://www.customs.gov.cn/customs/302249/2480148/5425109/index.html

3.Announcement of the Ministry of Commerce No. 35 of 2023 Announcement of the Ministry of Commerce on the extension of the Investigation on Trade Barriers in respect of Taiwans trade restriction measures against the Mainland

Issuance Date: 2023-10-09

Effective Date:2023-10-09

According to the foreign trade law of the Peoples Republic of China and the Ministry of Commerce "foreign trade barrier investigation rule" regulation, on April 12, 2023, the Ministry of Commerce 11th 2023 announcement, decided to Taiwan to mainland trade restrictions on trade barrier investigation.

In view of the complexity of the case, according to Article 32 of the Rules on Investigation of Foreign Trade Barriers, the Ministry of Commerce decided to extend the investigation period of the case by 3 months, that is, the deadline of the investigation period of the case is January 12, 2024.

LINK

http://www.mofcom.gov.cn/article/zcfb/zcblgg/202310/20231003444785.shtml

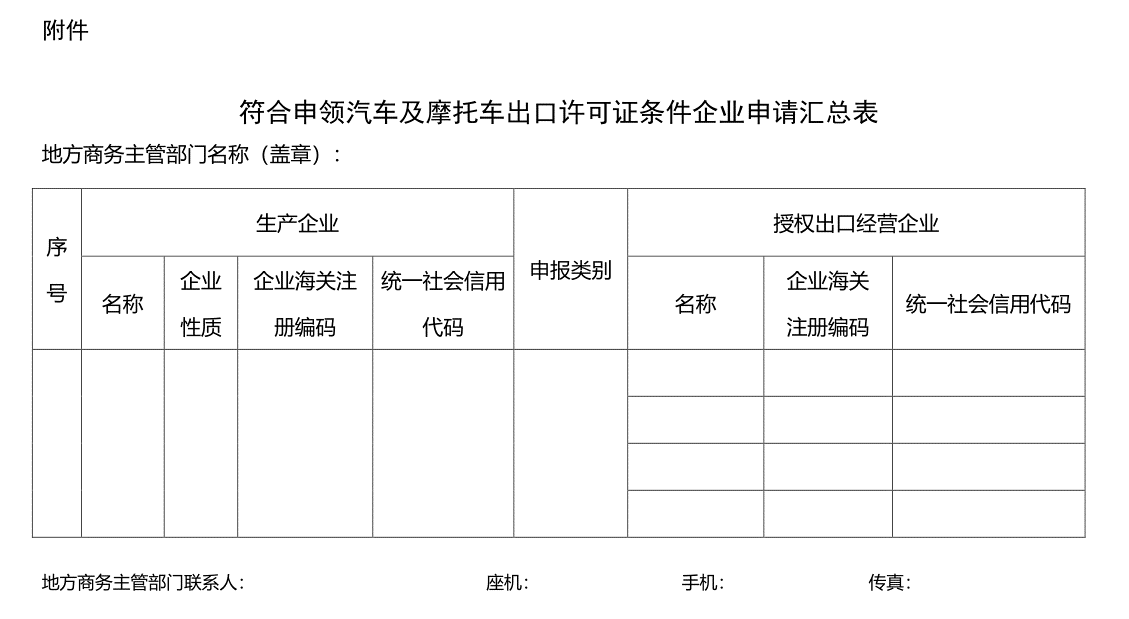

4.Commerce Office Trade Letter (2023) No. 470 Circular of the General Office of the Ministry of Commerce on the Application of Export License for Automobiles and Motorcycles in 2024

Issuance Date: 2023-09-15

Effective Date:2023-09-15

Provinces, autonomous regions and municipalities directly under the central government and cities under separate state planning, sinkiang production and construction corps departments of commercial administration:

In order to further standardize the export order of automobiles and motorcycles, according to the Notice of the General Administration of Customs, General Administration of Quality Supervision, Inspection and Quarantine of the Ministry of Commerce, Industry and Information Technology on Further standardizes the Export Order of Automobiles and Motorcycles (2012) No. 318), the relevant requirements of the application for export license of automobiles and motorcycles in 2024 are hereby notified as follows:

I. Form and procedure of declaration(I) In order to optimize the application process of enterprises and improve the level of digital management, we will carry out the work related to the application of automobile and motorcycle export license online this year.(2) production enterprise can log in car and motorcycle enterprises export license declaration system (https://ecomp.licence.org.cn), fill out the application form and upload the relevant documents, submit to the local competent commercial authority approval. Enterprises can check the review progress, public results and announcement list online.(3) the local competent commercial departments can log in automobile and motorcycle export licensing declare local management terminal (https://emanage.licence.org.cn), the system of local enterprises to declare at the beginning of nuclear materials, sorting summary the region enterprises filing status and report to the Ministry of Commerce. Local competent commercial departments can check the review progress, publicity results and announcement list in the system, make statistics and export the declaration situation of local enterprises, and conduct a second review on the modification materials submitted by enterprises with objections and report to the Ministry of Commerce during the publicity period.(4) Enterprises and local commercial authorities can download the user operation manual from the login page of the system.

II. Relevant requirements(I) The 2024 online application system will be launched on September 18, 2023. Local commercial authorities are requested to organize and guide local enterprises to do a good job in online declaration and truthfully and accurately fill in relevant information. The Ministry of Commerce will check the authenticity of the relevant declaration materials. If the enterprises are found to provide false materials, they will be notified, warned, suspended or cancelled for automobile or motorcycle export according to relevant regulations.(2) Local competent commercial departments shall complete the preliminary verification of the export license application materials of automobile and motorcycle enterprises and submit them online to the Ministry of Commerce before October 8, 2023, and submit the paper materials to the service hall of administrative affairs of the Ministry of Commerce (please indicate the words of "Export License Application Materials of automobile and Motorcycle" in the mail form).Postal address: Administrative Affairs Service Hall (Automobile and Motorcycle), Ministry of Commerce, No.2 East Chang an Avenue, Dongcheng District, BeijingTo and Tel: Wei Rihao 010-65197964(3) Paper materials submitted by local commercial authorities to the Ministry of Commerce include:1. General information of the application for export license by automobile and motorcycle enterprises in the region;2. Summary form of enterprise application (exported by Automobile and motorcycle Export License Declaration System, see attachment for template);3. If the competent commercial departments of relevant provinces and autonomous regions in the border areas recommend border trade enterprises, they shall provide relevant materials of the enterprises (not to apply through the online system for the time being) and the export operation situation of the recommended border trade enterprises in the previous year.

Please contact the License Bureau of the Ministry of Commerce (Tel: 010-84095747) if you need to fill in the system. For policy inquiries, please contact the Department of Foreign Trade, Ministry of Commerce (Tel: 010-65197368).

LINK

http://www.mofcom.gov.cn/article/zcfb/zcblgg/202309/20230903440856.shtml

5.Announcement No. 7 of 2023 Announcement of the Tariff Commission of The State Council on the Twelfth Exclusion and Extension List of Goods subject to tariffs from the United States and Canada

Issuance Date: 2023-09-11

Effective Date:2023-09-16

According to the tariff commission of the State Council on the tenth of American tariffs commodities exclude postponed listing announcement (tax committee announcement no. 1), 2023, the tenth of American tariffs commodities excluded postponed listing falls due on September 15, 2023. The Tariff Commission of The State Council has decided to extend the exclusion period for relevant commodities according to the procedures. The relevant matters are hereby announced as follows:

From September 16, 2023 to April 30, 2024, the goods listed in the Annex will continue to be exempted from the tariffs imposed by China in retaliation for the US 301 measures.

LINK

http://gss.mof.gov.cn/gzdt/zhengcefabu/202309/t20230913_3906830.htm

6.The US will continue to extend tariff exemptions on 352 Chinese imports and 77 anti-epidemic goods

Issuance Date: 2023-09-06

Effective Date:2023-09-06

The Office of the United States Trade Representative (USTR) announced on September 6 that it will further extend the Section 301 tariff exemption period for 352 Chinese imports that have been restored and 77 Chinese imports related to COVID-19 prevention, from September 30 to December 31 this year.

LINK

https://ustr.gov/about-us/policy-offices/press-office/press-releases/2023/september/ustr-extends-reinstated-and-covid-re lated-exclusions-china-section-301-tariffs

Policy Interpretation

According to previous media reports, in the name of "national security", Trump invoked "Section 301" (the common name of Section 301 of the US Trade Act of 1974) to impose tariffs on Chinese imports. During the Trump administration, more than 2,200 items were exempted from the tariffs, of which 549 were extended for a year, but all of the exemptions expired at the end of 2020. In October 2021, the USTR announced that it planned to re-exempt 549 Chinese imports from tariffs and sought public comment on the matter. Nearly half a year later, the UTRS issued a statement on March 23 last year, confirming 352 of the 549 Chinese imports that had been proposed to be re-exempted from tariffs. The exemption period has been extended several times since then.

The 352 items of Chinese imports include: Hot roller laminators, water filters, purifiers, garage switches, animal feeders and their accessories, electric motors, motor speed controllers, sensors, valves, aluminum electrolytic capacitors, connectors, electrogalvanized anodes, carbon dioxide analyzers and spare parts, scanners, thermostats designed for air conditioning or heating systems, polyethylene films, motorcycles (mopeds), crab meat, artificial stones Ink, catalyst, hydrofluorocarbon, man-made fiber duffle bag, silk fabric, woven dyed fabric, polypropylene fiber, non-woven fabric, motor vehicle rearview mirror, color digital camera for microscope and other commodities.

China always believes that the unilateral tariff measures imposed by the United States are not good for China, the United States and the world. As inflation continues to rise and global economic recovery faces challenges, we hope that the US will bear in mind the fundamental interests of Chinese and US consumers and producers, cancel all additional tariffs on China as soon as possible, and bring bilateral economic and trade relations back to the normal track at an early date.

7.Circular of the General Office of the Ministry of Transport on the Full Resumption of international cruise Transport (2023) No. 55

Issuance Date: 2023-09-19

Effective Date:2023-09-19

Tianjin, hebei, liaoning, Shanghai, jiangsu, zhejiang, fujian, shandong, guangdong, guangxi zhuang autonomous region and hainan province transportation hall (committee), directly under the maritime affair bureau:On the basis of the pilot resumption of international cruise transport at the cruise ports of Shanghai and Shenzhen, the relevant departments of business have decided to fully resume international cruise transport to and from cruise ports in China as of the date of this circular. The relevant matters are hereby notified as follows:

I. Make all preparations for the resumption of navigationInternational cruise ships carry a large number of passengers, spend a long time at sea and require high emergency response. Therefore, local governments should attach great importance to them and make solid preparations for the resumption of navigation to ensure the safety of peoples lives and property. The competent departments of transport in the places where the cruise ship ports of call shall, together with relevant departments, formulate an implementation plan for the resumption of international cruise transport and submit it to the local peoples governments for approval before proceeding with the resumption of international cruise transport. It shall, together with relevant departments, organize a review of the preparations for the resumption of cruise transport and port enterprises, which shall include the following contents:(1) Cruise transport and port enterprises shall have corresponding qualifications according to law.(2) Cruise ships shall meet the conditions for safety and seaworthiness. Cruise ships that have not carried passengers during the epidemic period shall conduct a non-operational voyage in accordance with relevant regulations before resuming operations and newly built cruise ships shall be put into operation, and a pre-sailing safety assessment shall be organized.(3) The cruise ship shall match the berthing capacity of the cruise port terminal (berth) to be docked.(4) Cruise transport and port enterprises shall, in accordance with relevant regulations, establish and improve safety emergency response and COVID-19 prevention and control systems and emergency plans, and equip them with necessary epidemic prevention materials.(5) The facilities and equipment at the customs clearance site shall meet the requirements of the cruise ship and its passengers for customs clearance inspection.

II. Strengthen emergency safety management and epidemic prevention and controlCruise transport has a major responsibility for safety, and we must firmly guard the bottom line and red line of production safety. Under the leadership of local governments and in accordance with relevant emergency plans and division of responsibilities, the competent transport departments of the places where cruise ships call should do a good job in emergency response, strengthen emergency management of cruise ports, establish an emergency liaison mechanism with cruise transport enterprises, urge them to strengthen safety inspection, and strictly prevent passengers from carrying dangerous goods and other prohibited items on board. Maritime administrative authorities should strengthen safety supervision of cruise ships, carry out flag state and port state supervision and inspection in accordance with regulations, carry out a safety inspection before the first voyage of cruise ships at the departure port, urge cruise transport enterprises to strengthen ship safety management and emergency drills, and strictly implement relevant safety regulations such as ship prohibition management. We will continue to implement the large-scale cruise rescue action plan and improve our emergency preparedness. Competent transport authorities and maritime administrative authorities in the places where cruise ships call should guide Chinese cruise transport companies to strengthen dynamic monitoring of ships, improve shore-based support capabilities, and ensure that emergency response can be "heard, seen and commanded"; In conjunction with relevant departments, they should urge and guide cruise transport and port enterprises to implement the requirements of the state and its territories on epidemic prevention and control according to their duties.

III. Strengthen management of the cruise transport marketThe competent transport authorities of the places where the cruise ship ports of call shall, together with relevant departments, manage the cruise transport market in accordance with the law, strengthen supervision before and after the event, and maintain market order; Guide cruise transport enterprises to enrich their products, optimize on-board services, and continuously improve the level of transport services; Guide cruise transport and port enterprises to implement the "Cruise Port Service Standards" together with relevant units, optimize the procedures for passengers entry, exit and boarding, and improve passengers service experience; We will urge cruise transport and port enterprises to implement the cruise ticket management system and the cruise operation statistics and investigation system. The competent departments of transport and maritime administration should urge cruise ships to use shore power in accordance with regulations.

Provincial transport authorities and relevant departments are requested to strengthen guidance and supervision on the resumption of navigation, timely coordinate and solve problems, promote the steady and healthy development of the international cruise transport market, and report the resumption of international cruise transport in their respective jurisdictions to the Ministry of Water Transport Bureau by the end of 2023.

LINK

https://xxgk.mot.gov.cn/2020/jigou/syj/202309/t20230919_3921649.html

Policy Interpretation

The competent transport departments of the places where the cruise ship ports of call shall, together with relevant departments, formulate an implementation plan for the resumption of international cruise transport, and proceed with the resumption after submitting the approval of the local peoples governments. It shall, together with relevant departments, organize a review of the preparedness of cruise transport and port enterprises for the resumption of cruise shipping.

Under the leadership of local governments and in accordance with relevant emergency plans and division of responsibilities, the competent transport departments of the places where cruise ships dock should do a good job in emergency response, strengthen emergency management of cruise ports, establish an emergency liaison mechanism with cruise transport enterprises, urge them to strengthen safety inspection, and strictly prevent passengers from carrying dangerous goods and other prohibited articles on board.

Maritime administrative authorities should strengthen safety supervision of cruise ships, carry out flag state and port state supervision and inspection in accordance with regulations, carry out a safety inspection before the first voyage of cruise ships at the departure port, urge cruise transport enterprises to strengthen ship safety management and emergency drills, and strictly implement relevant safety regulations such as ship prohibition management.

Cruise transport enterprises should be guided to enrich their line products, optimize on-board services, and continuously improve the level of transport services.

Guide cruise transport and port enterprises to implement the "Cruise Port Service Standards" together with relevant units, optimize the procedures for passengers entry, exit and boarding, and improve passenger service experience.

8.Ministry of Commerce Announcement No. 34 of 2023 Detailed Rules for the Implementation of Import Tariff Quotas on Sugar, wool and woolen slies in 2024

Issuance Date: 2023-09-25

Effective Date:2023-09-25

According to the Ministry of Commerce, National Development and Reform Commission in 2003 no. 4 (the "interim measures for management of import tariff quota of agricultural products"), the Ministry of Commerce developed the sugar import tariff quota of 2024 applications and distribution rules and the import tariff quota of wool and woolen sliver in 2024 management rules ", now make a public announcement.

LINK

http://www.mofcom.gov.cn/article/zcfb/zcblgg/202310/20231003444607.shtml

9.Announcement of the Ministry of Industry and Information Technology of the State Administration of Taxation No. 15, 2023 Announcement of the Ministry of Industry and Information Technology of the State Administration of Taxation on the issuance of the Catalogue of Non-Special Operation Vehicles with Fixed Devices Exempted from Vehicle Purchase Tax (the eleventh batch)

Issuance Date: 2023-09-01

Effective Date:2023-09-01

According to the Ministry of Industry and Information Technology of the taxation administration of the Ministry of Finance on a fixed device of transportation special operation vehicle vehicle purchase tax shall be exempted on policy announcement (35, 2020), the state administration of taxation of industry and information technology, special operation on a fixed device of transport vehicle announcement of vehicle purchase tax shall be exempted on administrative matters (2020) No. 20) in accordance with relevant provisions, the Catalogue of Non-transport Special Operation Vehicles with Fixed Devices Exempted from Vehicle Purchase Tax (eleventh batch) is hereby issued.

LINK

https://fgk.chinatax.gov.cn/zcfgk/c100012/c5213590/content.html

Policy Interpretation

I. Background of the announcementIn order to effectively implement the reform requirements of The State Council on optimizing the business environment, improve the level of tax service, improve the quality and efficiency of tax administration, and better safeguard the rights and interests of taxpayers, The Ministry of Finance, the State Administration of Taxation and the Ministry of Industry and Information Technology have formulated and issued the Announcement on Policies Related to Vehicle Purchase Tax Exemption for Non-Transportation Special Operation Vehicles with Fixed Devices (No.35, 2020). The State Administration of Taxation and the Ministry of Industry and Information Technology have formulated and issued the Announcement on Administrative Matters Related to Vehicle Purchase Tax Exemption for Non-Transportation Special Operation Vehicles with Fixed Devices (202 No. 20, 2020) to further optimize the vehicle purchase tax preferential policy management mechanism for non-transport special operation vehicles with fixed devices (hereinafter referred to as "special purpose vehicles"). For special purpose vehicles exempted from vehicle purchase tax, management is implemented through the Catalogue of Non-transport Special Operation Vehicles with Fixed Devices Exempted from Vehicle Purchase Tax (hereinafter referred to as the Catalogue), and taxpayers who purchase special purpose vehicles listed in the Catalogue can enjoy the policy of vehicle purchase tax exemption.

II. Basic information of this batch of CataloguesThis batch of catalogs is the fourth to be released in 2023, totaling the eleventh batch, involving a total of 260 models from 119 enterprises.

III. Issues to be explained

(1) How to apply for inclusion of qualified special purpose vehicles in the Catalogue?For the models applying for inclusion in the Catalogue, vehicle manufacturers, dealers of imported vehicles or individuals (hereinafter referred to as "applicants") shall submit the application materials for inclusion in the Catalogue through the "Management System for Vehicles with fixed Devices for Non-special Purpose Transportation Operations exempted from Vehicle Purchase Tax" of the Ministry of Industry and Information Technology.

(2) How to deal with failure to pass the technical examination?Failure to pass the technical examination refers to the situation where the applicant submits relevant materials through the declaration system, but the equipment center gives the conclusion of "fail" due to the failure to meet the "Technical Requirements for Non-special Transport Operation Vehicles with fixed Devices", incomplete submission of materials, incorrect filling and other reasons. For the case of failure to pass the technical examination, if the applicant does not agree with the technical examination conclusion of the equipment center, he/she can re-declare at any time through the declaration system; In the re-declaration, the applicant can put forward his own opinions on the technical examination conclusion of the equipment center, and provide corresponding supporting materials; The equipment center shall give the technical review conclusion again. If the applicant still does not agree with the conclusion of the re-examination of the equipment Center, he/she can consult, suggest or complain through the public service telephone platform 12381 of the Ministry of Industry and Information Technology, or report the relevant problems to the Ministry of Industry and Information Technology in the form of a letter, and the Ministry of Industry and Information Technology will deal with it according to the procedures.

(3) How to handle tax exemption for special vehicles listed in the Catalogue?According to the regulations, for the models listed in the Catalogue, the applicant may mark the tax-free mark in the electronic information of the vehicles produced. The tax authorities shall handle the formalities for tax exemption of vehicle purchase tax for taxpayers according to the tax exemption mark and other materials required to be provided for tax declaration of vehicle purchase tax.For example: Company A will produce A special vehicle on August 21, 2023. The eleventh batch of Catalogue issued by the State Administration of Taxation and the Ministry of Industry and Information Technology contains the models of the vehicles mentioned above. Company A will mark the tax-free mark in the vehicle electronic information of the vehicles sold.

(4) How to handle tax exemption for special purpose vehicles that have been sold before the release of the Catalogue?According to the regulations, for special purpose vehicles that have been sold before the release of the Catalogue, the applicant can mark the duty-free logo in the vehicle electronic information of the sold vehicles and re-upload it after the model of the sold vehicles is listed in the Catalogue. Taxpayers may apply for tax exemption with the competent tax authorities by virtue of the tax exemption mark and other materials required to be provided for the tax declaration of vehicle purchase tax.

For example, Company A sold A vehicle not listed in the Catalogue to taxpayer B on August 10, 2023. Company A did not mark the tax exemption mark when uploading the electronic information of the vehicle. After that, the 11th batch of Catalogue issued by the State Administration of Taxation and the Ministry of Industry and Information Technology contains the models of the vehicles sold above. After the 11th batch of Catalogue issued by the State Administration of Taxation and the Ministry of Industry and Information Technology, Company A can modify the electronic information of the vehicles purchased by taxpayer B, mark the duty-free mark and re-upload it. B taxpayer can enjoy the tax-free policy according to law by virtue of the tax-free mark and other materials.

(5) How to handle the inclusion of special vehicles in the Catalogue after taxpayers pay vehicle purchase tax?After the implementation of the "Catalog" management, if the taxpayer purchases a special vehicle and pays the vehicle purchase tax, and then the special vehicle is listed in the "Catalog", the applicant can mark the tax-free logo in the vehicle electronic information of the sold vehicle and upload it again after the model of the vehicle is listed in the "Catalog". The taxpayer can apply for tax refund to the competent tax authorities by virtue of the tax-free mark and other information required to be provided for the tax declaration of vehicle purchase tax. The competent tax authorities shall refund the tax already paid by the taxpayer according to law.

For example: Company A sold A vehicle not included in the Catalog to taxpayer B on August 5, 2023, and taxpayer B paid the vehicle purchase tax after purchasing the vehicle. After that, the eleventh batch of Catalog issued by the State Administration of Taxation and the Ministry of Industry and Information Technology included the models of the vehicles sold above. After the eleventh batch of Catalog issued by Company A, After the release of the catalogue, the electronic information of the vehicle purchased by taxpayer B can be modified, marked with the tax-free mark and re-uploaded. B taxpayer can apply for tax refund to the competent tax authority by virtue of the tax exemption mark and other materials.

10.Announcement of the State Administration of Taxation of the Ministry of Finance No. 69 of 2023 Announcement of the State Administration of Taxation of the Ministry of Finance on continuing to exempt waste mineral oil recycled oil products from consumption tax

Issuance Date: 2023-09-27

Effective Date:2023-09-27

To continue to support to promote comprehensive utilization of resources and environmental protection, and is now on the recycling of waste mineral oil as raw material to produce lube base oil, gasoline, diesel and other industrial oil shall be exempted from the consumption tax policy announcement is as follows:

I. Waste mineral oil refers to the waste lubricant that is replaced by machinery and equipment in the field of industrial production and transportation equipment such as automobiles and ships after their use has lost or reduced efficacy.

II. The lubricating oil base oil, gasoline, diesel and other industrial oils produced by taxpayers using waste mineral oil shall be exempted from consumption tax, and the following conditions shall be met at the same time:

(1) The taxpayer must obtain the Hazardous Waste (Comprehensive) Business License issued by the ecological environment department, and the approved production and business scope on the certificate shall include the words "utilization" or "comprehensive business". A taxpayer whose scope of production and operation is "comprehensive operation" shall also provide the materials issued by the ecological environment department that issues the "Hazardous Waste (Comprehensive) Operation License" that can prove that the scope of production and operation includes "utilization".

When applying for the record of exemption from consumption tax, the taxpayer shall simultaneously submit the pollutant discharge standards to be implemented by the taxpayer determined by the ecological environment department at the place where the pollutants are discharged, as well as the certification materials issued by the ecological environment department at the place where the pollutants are discharged within the previous 6 months that the pollutant discharge of the taxpayer meets the above-mentioned standards.

The waste mineral oil recovered by the taxpayer shall have the Hazardous Waste Transfer Form that can show its name, characteristics, quantity, date of acceptance and other items.

(2) The weight of waste mineral oil in raw materials for production must account for more than 90%. The finished product must include lubricating oil base oil, and the lubricating oil base oil produced by each ton of waste mineral oil shall not be less than 0.65 tons.

(3) Products produced from waste mineral oil and products produced from other raw materials shall be accounted for separately.

III. When selling tax-free oil products, taxpayers conforming to Article 2 of this announcement shall indicate the name of the product on the special VAT invoice, and add "(waste mineral oil)" after the name of the product.

IV. Taxpayers in accordance with Article 2 of this announcement shall continuously process and produce lubricating oil from lubricating oil base oil produced by waste mineral oil, or taxpayers (including taxpayers in accordance with Article 2 of this announcement and other taxpayers) shall purchase lubricating oil base oil produced by waste mineral oil for processing and production of lubricating oil, When declaring the consumption tax of lubricating oil, the consumption tax shall be calculated and paid according to the balance of the quantity of lubricating oil sold in the current period minus the quantity of lubricating oil base oil consumed in accordance with the provisions of this announcement.

V. For taxpayers who fail to meet the corresponding pollutant discharge standards or whose Hazardous Waste (Comprehensive) Business License has been cancelled, their qualification to enjoy the consumption tax exemption policy stipulated in this announcement shall be cancelled from the date of the occurrence of the illegal discharge act or the date of the cancellation of the Hazardous Waste (Comprehensive) Business License, and they shall not apply again within three years. Taxpayers who have applied for and applied for tax exemption since the date of illegal discharge shall be pursued for payment.

VI. The TAX AUTHORITIES at all levels shall take strict measures to strengthen the dynamic supervision over the taxpayers who enjoy the consumption tax exemption policy stipulated in this announcement. Where it is verified that a taxpayer fraudulently and fraudulently enjoys the policy of exempting consumption tax as stipulated in this announcement, the tax authorities shall recover the tax exemption he/she has defrauded and cancel his/her qualification to enjoy the policy of exempting consumption tax as stipulated in this announcement from the year in which the aforesaid violation of laws and regulations occurs, and the taxpayer shall not apply again within three years.The date of illegal discharge refers to the date on which the taxpayer fails to meet the standards for pollutant discharge, which has been verified and confirmed by the ecological environment department in the place where pollutants are discharged.

VII. This announcement shall be implemented until December 31, 2027.

LINK

https://fgk.chinatax.gov.cn/zcfgk/c102416/c5214575/content.html

11.Circular of the Ministry of Finance of the State Administration of Taxation and the Peoples Bank of China on Further strengthening the Administration of Handling Fees for Tax withholding and collection

Issuance Date: 2023-09-24

Effective Date:2023-10-01

The state administration of taxation of all provinces, autonomous regions and municipalities directly under the central government, cities under separate state planning, tax bureau, the provinces, autonomous regions and municipalities directly under the central government, cities under separate state planning departments (bureau), the Peoples Bank of China, the provinces, autonomous regions and municipalities directly under the central government, cities under separate state planning branch:

In order to further regulate and strengthen the management of tax handling fees for withholding and payment, collection and payment and entrusted collection (hereinafter referred to as the "Three Generations"), pursuant to the provisions of the Budget Law of the Peoples Republic of China and the Tax Collection and Administration Law of the Peoples Republic of China and other relevant laws and administrative regulations, the circular regarding further strengthening the management of tax handling fees for the "Three Generations" is as follows:

I. Scope of the "three Generations"

(1) Withholding and payment refers to the act of withholding on behalf of the tax authority the income paid to the entity or individual liable for tax payment and releasing the income to the tax authority when the tax laws and administrative regulations have clearly stipulated that the entity or individual liable for tax payment is making payment.

(2) Collection and payment on behalf of tax authorities refers to the act of collecting and paying on behalf of tax authorities the income paid to units and individuals with tax obligations which have been clearly stipulated by tax laws and administrative regulations.

(3) Entrustment of tax collection refers to the act of entrusting relevant units and persons to collect sporadic, dispersed and non-local taxes on behalf of the tax authorities in accordance with the requirements of the Law of the Peoples Republic of China on the Administration of Tax Collection and the Detailed rules for its implementation, which are conducive to tax control and convenient payment of taxes, and in accordance with the principles of voluntary, simple collection, enhanced administration and entrustment according to law, as well as the relevant regulations of the State.

II. "Three-generation" administrationTax authorities shall carry out the work of "three generations" in strict accordance with the relevant provisions of the Law of the Peoples Republic of China on the Administration of Tax Collection and its implementation rules. Tax authorities shall, in accordance with laws, administrative regulations and the relevant provisions of the State Administration of Taxation, determine the "three generations" units or individuals, and shall not, on their own, expand the scope of "three generations" or increase the proportion of tax handling fees paid by the "three generations".

(1) The tax authorities shall, in accordance with the relevant provisions of the State Administration of Taxation, register the withholding agents who are responsible for the withholding and payment of taxes or the collection and payment of taxes.Tax authorities may not require any entity or individual to perform any tax withholding or collection obligations for which the laws or administrative regulations do not provide for such obligations.

(2) Tax authorities shall determine the scope of entrusted tax collection in strict accordance with laws, administrative regulations and the relevant provisions of the State Administration of Taxation on entrusted tax collection, and shall not entrust others to collect the tax that has been determined by laws and administrative regulations.

(3) For the "three generations" of tax service fees to be paid in proportion, the tax authorities shall, in determining the proportion of service fees for the "three generations" of units or individuals, take into full account the business volume, work cost and other factors of the "three generations" of units or individuals from the perspective of reducing tax costs, determine a reasonable proportion of service fees to be paid. The limit of service fee payment may be set within the scope of the corresponding prescribed payment proportion as required.

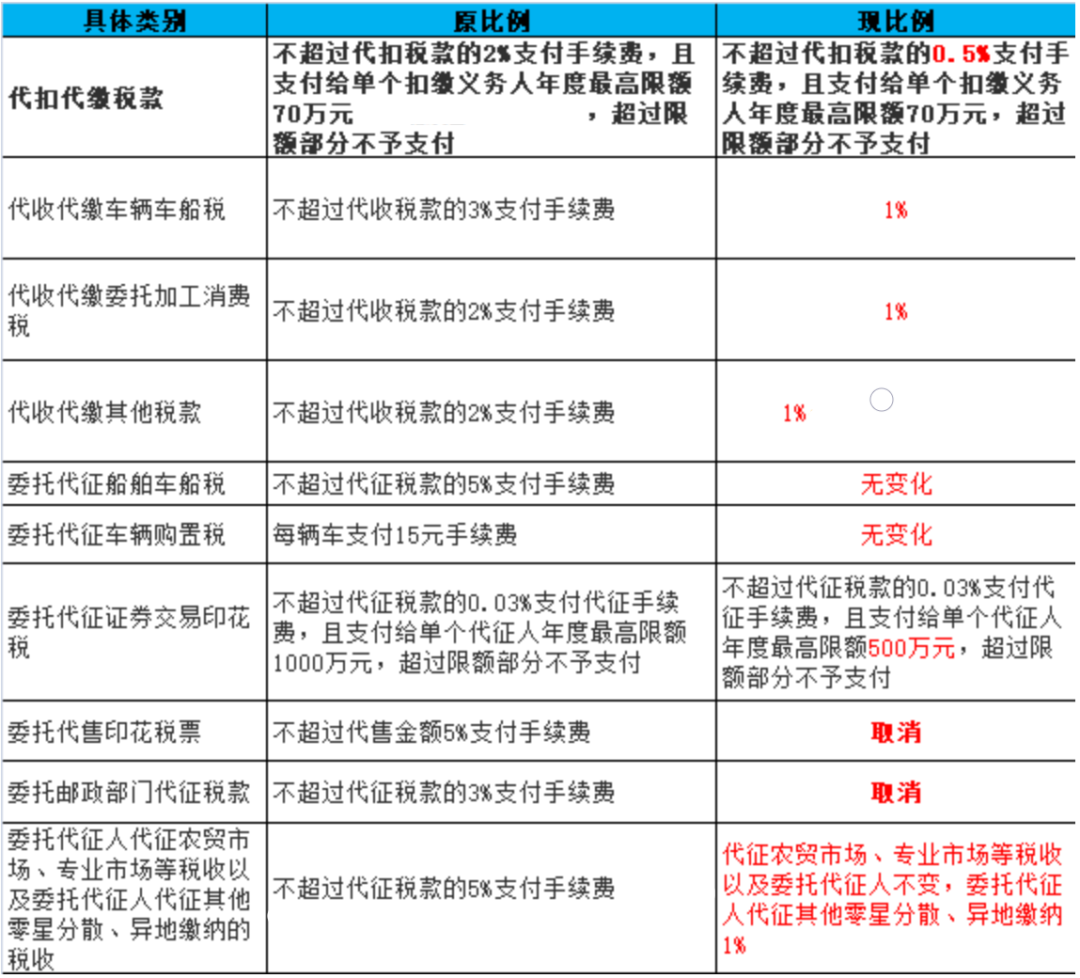

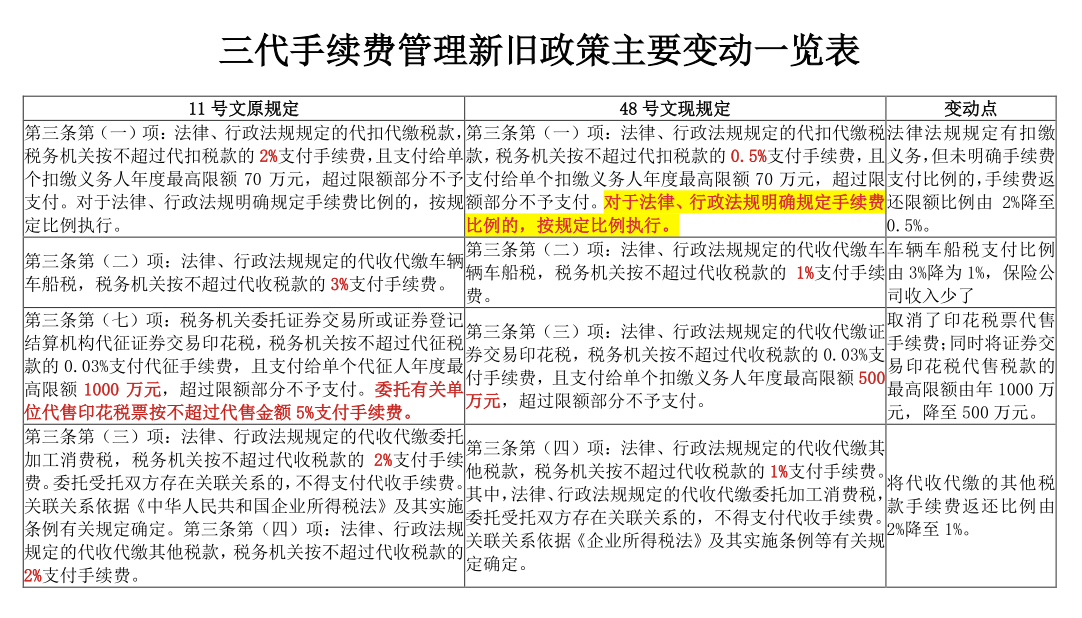

III. Proportion and limit of "three generations" tax service fee payment

(1) For the tax withheld and paid as prescribed by laws and administrative regulations, the tax authorities shall pay a handling fee of no more than 0.5% of the tax withheld and pay the maximum annual limit of 700,000 yuan to a single withholding agent. The part exceeding the limit shall not be paid. Where the proportion of handling fee is specified by laws and administrative regulations, the prescribed proportion shall be applied.

(2) For the collection and payment of vehicle and vessel tax as prescribed by laws and administrative regulations, the tax authorities shall pay the handling fee not exceeding 1% of the tax collected on behalf of the tax authorities.

(3) For the collection and payment of securities transaction stamp tax as stipulated by laws and administrative regulations, the tax authorities shall pay a handling fee not exceeding 0.03% of the tax collected on behalf of the agency, and the maximum annual limit for payment to a single withholding agent shall be RMB 5 million yuan, and the part exceeding the limit shall not be paid.(4) For the collection and payment of other taxes on behalf of the tax authorities as stipulated by laws and administrative regulations, the tax authorities shall pay a commission fee of no more than 1% of the tax collected on behalf of the tax withholding agents. For the collection and payment of consumption tax on behalf of processing as stipulated by laws and administrative regulations, no commission fee shall be paid if there is a related relationship between the entrusting parties. The related relationship shall be determined in accordance with the Enterprise Income Tax Law and its implementation regulations and other relevant provisions.

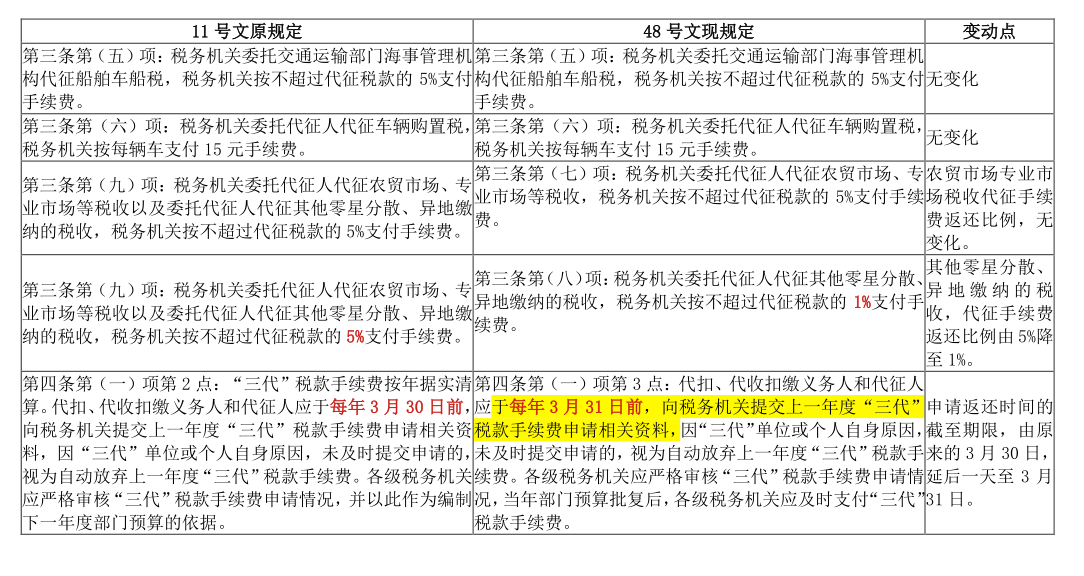

(5) The tax authority entrusts the maritime administration authority of the transport department to collect the vehicle and vessel tax on behalf of the vessel, and the tax authority shall pay the handling fee not exceeding 5% of the tax collected on behalf of the vessel.

(6) When the tax authority entrusts a tax collector to collect the vehicle purchase tax on his behalf, the tax authority shall pay a handling fee of 15 yuan per vehicle.

(7) When the tax authorities entrust a tax collector to collect taxes on behalf of the farmers market, specialized market, etc., the tax authorities shall pay the handling fee not exceeding 5% of the tax collected on behalf of the tax authorities.

(8) The tax authorities shall pay a commission of no more than 1% of the tax collected on behalf of the tax authorities who entrust a tax collector to collect other taxes that are scattered and paid in different places.

IV. Administration of tax service fees for the "Three generations"

(1) Budget management

1. Tax service fees for the "three generations" shall be included in budget management, and unified arrangements shall be made by the government through budget expenditures. Where laws and administrative regulations provide otherwise, such provisions shall be followed.

2. The tax authorities at all levels shall, in accordance with the relevant procedures and requirements of departmental budget preparation, prepare and report the budget of tax handling fees for the "three generations". The budget for surcharges of education fees and local education surcharges shall be prepared according to the proportion of the surcharges of positive taxes transferred by withholding, collecting and collecting on behalf of tax authorities.

3.Withholding and collection The withholding agent and the collector shall submit the relevant materials of the application for the "three generations" tax service fee of the previous year to the tax authority before March 31 of each year. If the application is not submitted in time due to the reasons of the "three generations" unit or individual, it shall be deemed to have automatically given up the "three generations" tax service fee of the previous year. The tax authorities at all levels shall strictly examine the application of the "three generations" tax handling fee, and pay the "three generations" tax handling fee in time after the approval of the budget of the current year.

4. If the withholding agent and the agent terminate the withholding obligation or the relationship between the agent and the agent within the year, the agent and the agent shall submit the application materials for the service fee to the tax authority within 3 months after the termination, and the tax authority shall handle the settlement of the service fee.

5. If the current years budget for tax handling fee of "three generations" is insufficient, it shall be made up in the next years budget; The carry-over part shall be reserved for the next year; The remaining part shall be handed over to the finance according to relevant regulations.

6. Tax authorities at all levels should strengthen the performance management of the "three generations" tax commission budget, set performance targets scientifically, improve performance evaluation methods, improve the quality of performance evaluation, and strengthen the application of performance evaluation results.

(2) Accounting management

1. Tax authorities at all levels shall, in accordance with relevant regulations on the accounting of administrative institutions, make timely, comprehensive and complete accounting of the "three generations" of tax handling charges.

2. Tax authorities at all levels shall, in accordance with the relevant requirements for the preparation and examination of the final accounts of the departments, truthfully, accurately, comprehensively and timely prepare and report the final accounts of tax fees of the "three generations", and do a good job in the examination of the final accounts.

(3) Payment management

1. The tax authorities shall pay the handling fee for the "three generations" of taxes in accordance with the centralized payment system of the Treasury and the provisions of this Circular.

2. The tax authorities shall not pay the "three generations" tax handling fee to any entity or individual that fails to perform the withholding, collection and collection obligations in accordance with the provisions of laws, administrative regulations or entrusted collection agreements.

3. No commission fee shall be paid for the entrustment of tax collection between tax authorities.

(4) Supervision and administration

1. If the tax and financial departments and their staff violate the provisions of this Notice or engage in other acts of abuse of power, dereliction of duty, malpractice for personal gains and other violations of law and discipline in the administration of tax fees for the "three generations", they shall be investigated for relevant responsibilities according to law; If the act constitutes a crime, criminal responsibility shall be investigated according to law.

2. The tax authorities at all levels shall strengthen the inspection and audit on the use and management of the "three generations" tax service fees, and shall accept the supervision and inspection of the financial and audit departments.

3. Unless otherwise provided for by laws and administrative regulations, tax authorities at all levels shall not directly withdraw service fees from taxes or return them to the Treasury, and state treasuries at all levels shall not return service fees for the "three generations" of taxes.

This notice shall take effect from October 1, 2023. The Circular of the Peoples Bank of China of the State Administration of Taxation of the Ministry of Finance on Further Strengthening the Administration of Handling Fees for Tax Withholding and Collection (Caixin No. 11, 2019) shall be repealed simultaneously.

LINK

https://fgk.chinatax.gov.cn/zcfgk/c102424/c5214506/content.html

Policy Interpretation

12.Single Window Cargo Declaration September 13, 2023 version

Issuance Date: 2023-09-13

Effective Date:2023-09-13

According to the General Administration of Customs business requirements, to update goods declaration system optimization:

1. Adjust the required requirements for the column of "Production date" in the commodity form of import declaration form. When the license category in the column of "Product qualification" in the commodity form of import declaration form contains 519 certificate, the column of "production date" in the commodity form of import declaration form cannot be empty.

2. Adjust the rules for filling in the column of "Production Date" in the commodity form of import Declaration, and the specific rules are as follows:(1) If the production date is a specific day, only 8 digits are allowed to fill in, and the format is year (4 digits), month (2 digits) and day (2 digits), such as 20230111.(2) If the production date is a certain period of time, the two production dates shall be divided by a half-angle horizontal line "-", such as 20230111-20230310.(3) If the same 519 certificate involves more than one production date, use the English semi-horn semicolon "-" during the production date; Split, e.g. 20230111; 20230310.(4) The production date of the current product between different 519 certificates is divided by the English half-angle slash "/", such as 20230111/20230310.(5) If there are multiple 519 certificates for the current commodity, and each 519 certificate has multiple production dates and involves time periods, the example format of production date is as follows: 20230111; 20230113-20230310/20230222-20230312; 20230412

3. The number of "production date" in the commodity table of the import declaration form should be consistent with the number of 519 certificates in the column of "Product qualification" in the table body.4. Add the "Production date" display field in the "Product qualification" column of the commodity table body of the import declaration, which is only for display and cannot be modified.5. When applying for modification of import declaration form, the modification requirements of "Production Date" column in the commodity form of declaration form shall be the same as above.

LINK

https://www.singlewindow.cn/#/detail?breadNum=bc13&articleId=dec001202309130001

13.Notice on CQC-C0101-2014 "Compulsory Product Certification implementation rules Wire and cable products" revision

Issuance Date: 2023-09-11

Effective Date:2023-09-15

All relevant units:China Quality Certification Center (English abbreviation CQC) recently on CQC-C0101-2014 "mandatory product certification implementation rules wire and cable products" has been revised, involving product categories: 0104, 0105, the revised detailed documents please see the attachment.

I. The main content of the revision

1. Article 4.2.1 adds the content of testing laboratory selected by the certification client.

2. Add the content of "double random" mechanism for initial factory inspection in Clause 4.3.3.

3. Article 4.4 Product consistency confirmation inspection is amended as follows: In principle, the original type test laboratory shall be sent for product consistency confirmation inspection.

4. Article 5.2 adds the content of the certification results of the quality management system of the enterprise.

5. Modify Annex 1 wire and cable products mandatory certification type sample requirements, while adding the requirements of note 4.

6. Modify Annex 2 List of key raw materials for mandatory certification of wire and cable products.

7. modify Annex 5 wire and cable products mandatory certification factory quality control testing requirements, GB/T5013 standard part, JB/T8735 standard part add note

(4) for external commissioned irradiation processing, mechanical properties and thermal extension test before aging to confirm the inspection frequency should be batch by batch; Delete GB/T12528 standard part.

II Implementation requirements1. The revision of the rules does not involve the conversion of the CCC certificate issued.2. These rules will be implemented from September 15, 2023. If you have any questions, please contact the Fourth Department of Product Certification (010-83886556/6926/6856).

LINK

https://www.cqc.com.cn/www/chinese/c/2023-09-11/560760.shtml

14.Notice on the implementation of the new standard and implementation rules for the Safety certification of Fixed Capacitors used to suppress electromagnetic interference of power Sources (001007 category)

Issuance Date: 2023-09-25

Effective Date:2023-09-25

All relevant units:GB/T 6346.14-2023 "Fixed capacitors for use in electronic equipment - Part 14: Sub-specification Fixed Capacitors for Power Supply Electromagnetic Interference suppression (hereinafter referred to as the "new standard") has been released on March 17, 2023, and will be implemented and replace GB/T 6346.14-2015 (hereinafter referred to as the "old standard") from October 1, 2023. China Quality Certification Center (CQC) has revised the certification rule CQC11-471115-2016 "Safety Certification Rules for Fixed Capacitors Used to Suppress Electromagnetic Interference of Power Sources" related to this standard, involving the small class number 001007. The relevant requirements for the revision of the rules and implementation are hereby notified as follows:

I. Main amendments to the Rules1. CQC11-471115-2023 instead of CQC11-471115-2016;2. Modify 4.2.1 certification basis standard, GB/T 6346.14-2015 updated to GB/T 6346.14-2023.

II. The implementation of the new standard requirements:1. From the date of this notice, CQC will adopt the new standard implementation certification and issue the new standard certification certificate.2. For the products that have been certified according to the old version of the standard, the old version of the standard certification certificate holder should submit to our organization in time to convert the new version of the standard certification application, and after the implementation date of the standard, before the end of the first follow-up inspection, complete the product confirmation and certificate replacement work according to the new version of the standard (the main differences and test requirements of the new version of the standard see the attachment), All the old version of the standard certificate conversion work should be completed before September 30, 2024 at the latest; If the conversion fails to be completed within the time limit, our center will suspend the old standard certificate; If the conversion is not completed by December 31, 2024, our center will revoke the old standard certificate.3. For the certified products that have been delivered before October 1, 2023, and are no longer in the market, there is no need to carry out the certificate conversion.4. The relevant designated laboratories should report to our center as soon as possible has the new version of the standard testing ability, and should be timely through the new version of the standard laboratory accreditation and accreditation of the situation on record.From now on, the product certification department of our center begins to accept the certification application of the new standard. Enterprises can submit the certification application through the official website of China Quality Certification Center (www.cqc.com.cn). For specific matters, please contact the engineer of the product certification department:Contact person: Tao Ke (010-83886674)Xu Deng (010-83886381)Zhang Yi (010-83886589)

LINK

https://www.cqc.com.cn/www/chinese/c/2023-09-25/560789.shtml

15.Notice on the renewal of Implementation Rules for Certification of Wind Turbine Blades for Wind Turbines (Category 030011)

Issuance Date: 2023-10-10

Effective Date:2023-10-05

Each related enterprise:China Quality Certification Center (English abbreviation CQC) recently updated CQC34-461315-2015 "Wind Turbine Blade Certification Implementation Rules", involving small class number: 030011. The specific information is as follows:

I. Main amendments to the rules:1. Add IEC 61400-1-2019 and IEC 61400-22:2010;2. Replace IECRE OD-501:2018 with IECRE OD-501:2022 Ed 3.0.

II Implementation requirements1. From October 5, 2023, CQC will adopt the revised implementation rules for certification and issue certification certificates. Enterprises can submit certification applications through the CQC website. For specific matters, please contact relevant engineers in the new Energy Product Certification Department of CQC.Contact person 1: Li Fu Tel: 010-83886033, 15011334963Contact person 2: Ren Wei Tel: 010-83886370This revision does not involve the change of issued certificates.

LINK

https://www.cqc.com.cn/www/chinese/c/2023-10-10/560827.shtml

31019002000120

31019002000120

返回新闻列表

返回新闻列表