021-50368000

021-50368000

Import Trade Statistics

The total value of Chinas imports and exports in March 2024 was US$500.81 billion, up 24.9 per cent sequentially compared with February this year, and down 5.1 per cent sequentially compared with March last year; for exports, the value of exports in March was US$279.68 billion, up 27.0 per cent sequentially compared with February this year, and down 7.5 per cent sequentially compared with March last year; for imports, the value of imports in March was US$2 2,211.3 billion U.S. dollars in March, compared with February this year, a year-on-year increase of 22.4 per cent, compared with March last year, a decrease of 1.9 per cent. The goods trade surplus was US$58.55 billion, with a cumulative total of US$183.66 billion from January to March.

Chinas imports of electromechanical products in March 2024 were 572.26 (exports 1,178.03) billion yuan, and the cumulative imports of electromechanical products from January to March were 1,544.72 (exports 3,394.15) billion yuan, an increase of 9.6 (export growth of 6.8) per cent compared with the same period last year; among them, 429.7 (exports 23.02) billion of integrated circuits were imported in March, the valued at RMB 222.17 (exports 103.79) billion, and imports of RMB 610.1 (exports 264.49) billion from January to March, an increase of 14.3 (exports up 24.2) per cent compared with last year.Medical equipment imports of RMB 8.53 (exports 11.05) billion in March, and imports of RMB 21.53 (exports 31.17) billion yuan, down 6.8 (exports up 7.2) per cent from a year earlier.

1.General Administration of Customs Announcement No. 30 of 2024 (Announcement on the Adjustment of Declaration Requirements for Import and Export Goods Declarations)

Issuance Date: 2024-03-14

Effective Date: 2024-04-10

In order to further regulate the declaration behaviour of consignees and consignors of import and export goods, and to streamline the relevant declaration columns, the General Administration of Customs has decided to adjust the relevant columns of the "Customs Declaration of Goods Imported (Exported) by the Customs of the Peoples Republic of China" and the "Customs Recorded List of Goods Imported (Exported) by the Customs of the Peoples Republic of China", as well as some of the declaration items and their reporting requirements as follows:

I. Amendments to Articles 25 and 26 in the Specification for Filling Customs Declarations for Import and Export Goods of the Customs of the Peoples Republic of China (issued by the General Administration of Customs under Announcement No. 18 of 2019).

Article 25 of the "gross weight (kg)" filling requirements from "fill in the import and export of goods and their packaging materials and the weight of the sum of the unit of measurement in kilograms, less than one kilogram is reported as 1. " Revised to "Report the sum of the weight of imported and exported goods and their packaging materials, the unit of measurement is kilograms, less than one kilogram is accurate to two decimal places."

Article 26 of the "net weight (kg)" fill in the requirements from "fill in the import and export of the gross weight of the goods minus the weight of the outer packaging materials, that is, the actual weight of the goods themselves, the unit of measurement is kilograms, less than a kilogram of fill in as 1. ." Revised to "Report the gross weight of imported and exported goods minus the weight of the outer packaging materials, i.e. the actual weight of the goods themselves, with the unit of measurement being kilograms, and with less than one kilogram reported to two decimal places."

II. The deletion of "inspection and quarantine acceptance authority" "port inspection and quarantine authorities," "the licensing authority" and other three declarations.

III. "Destination inspection and quarantine authorities" declaration item name adjustment to "destination customs". The declaration column for the conditional required, if the relevant laws, administrative regulations, international treaties or trade contracts provide for the implementation of inspection and quarantine or supervision of imported goods, the declaration is required. According to the implementation of inspection and quarantine of the destination customs, fill in the customs regulations "Customs Code Table" in the corresponding destination customs name and code.

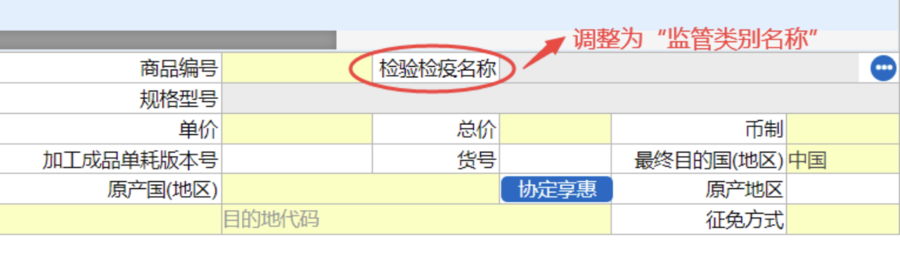

IV. "Inspection and quarantine name" declaration project name adjusted to "regulatory category name", fill in the requirements remain unchanged.

This Notice shall come into operation on 10 April 2024.

LINK

http://www.customs.gov.cn/customs/302249/302266/302267/5758885/index.html

Policy Interpretation:

The scope of use of this announcement includes customs declarations and filing lists.

I. Article 25 of the General Administration of Customs Announcement No. 18 of 2019 (hereinafter referred to as "Announcement No. 18") stipulates that the gross weight in the header of the table shall be filled in according to 1kg if it is less than 1kg, that is, it shall not be less than 1kg. This Notice specifies that the gross weight at the head of the table can be filled in as less than 1kg, accurate to 2 decimal places. For example, 0.563kg is to be entered as 1kg in accordance with Bulletin 18 and 0.56kg in accordance with this Bulletin.

Article 26 of Circular No. 18 stipulates that the net weight at the head of the table, if it is less than 1 kg, should be entered as 1 kg, i.e. not less than 1 kg. This Notice specifies that the net weight at the head of the table can be filled in as less than 1kg, accurate to 2 decimal places. For example, 0.563kg is to be entered as 1kg in accordance with Bulletin 18 and 0.56kg in accordance with this Bulletin.

Note: This announcement is for the net weight of the "head" of the table, the net weight of the body of the table is still in accordance with the provisions of Announcement No. 18.

II. The deletion of "inspection and quarantine acceptance authority" "port inspection and quarantine authorities," "the licensing authority" and other three declarations.

Interpretation: Cancellation of the content in the red box in the figure below on the Customs Declaration page:

III. "Destination inspection and quarantine authorities" declaration item name adjustment to "destination customs". The declaration column for the conditional required, if the relevant laws, administrative regulations, international treaties or trade contracts provide for the implementation of inspection and quarantine or supervision of imported goods, the declaration is required. According to the implementation of inspection and quarantine of the destination customs, fill in the customs regulations "Customs Code Table" in the corresponding destination customs name and code.

Interpretation: The content of the red circle on the customs declaration is amended to read "Customs of destination".

IV. "Inspection and quarantine name" declaration project name adjusted to "regulatory category name", fill in the requirements remain unchanged.

Interpretation: The content of the red circle on the customs declaration is amended to read "Name of regulatory category".

2.General Administration of Customs Announcement No. 32 of 2024 (Announcement on Implementation of Customs Advance Ruling Extension and Other Related Matters)

Issuance Date: 2024-03-15

Effective Date: 2024-05-01

In order to further enhance the predictability of import and export trade activities, and to promote the optimisation of the business environment, in accordance with the relevant provisions of the Interim Measures for the Administration of Advance Rulings of the Customs of the Peoples Republic of China (Decree No. 236 of the General Administration of Customs, hereinafter referred to as the "Interim Measures for the Administration of Advance Rulings"), the implementation of the Customs commodity classification, price and origin advance rulings on extension of the relevant matters are announced as follows:

I. Implementation of measures for the renewal of advance rulings upon application

(a) On the premise that there is no change in the categories of customs affairs, basic information on commodities, and matters to be pre-determined in the Decision on Advance Ruling of the Customs of the Peoples Republic of China (hereinafter referred to as the Decision on Advance Ruling), the original applicant may, within 30 to 90 days prior to the expiry date of the Decision on Advance Ruling, apply to the Customs Service issuing the Decision on Advance Ruling to extend the validity date of the Decision on Advance Ruling. Application.

(b) The Customs shall, within 30 days from the date of receipt of the applicants application for extension of the Decision on Advance Ruling, complete the examination and issue a new Decision on Advance Ruling, which shall be valid within 30 days from the date of receipt of the applicants application for extension of the Decision on Advance Ruling. Interim Measures for the Administration of Advance Rulings" and other relevant laws, administrative regulations, customs rules and regulations, as well as announcements of the General Administration of Customs on matters of commodity classification, price and origin, etc., to complete the examination and issue a new "Advance Ruling Decision Letter", which is valid for three years. From the effective date of the newly issued Advance Ruling Decision Letter, the original Advance Ruling Decision Letter will automatically expire.

(c) In any of the following cases, the Customs shall not accept the application for extension and shall return the application with reasons:

1. Where the Pre-Determination Decision has lapsed or been cancelled;

2. Changes in the applicants name, enterprise code and unified social credit code;

3. Failure to submit the application within the prescribed period;

4. After the issuance of the Advance Ruling Decision, the relevant customs regulations and announcements of the General Administration of Customs have made clear provisions on the relevant customs affairs covered by the Advance Ruling Decision.

II. Application by pilot overseas exporters or producers for advance rulings on commodity classification, price and origin

(a) Overseas exporters or manufacturers who have signed a contract of sale of goods with the consignee of imported goods (hereinafter referred to as the consignee) in the China (Shanghai) Pilot Free Trade Zone (including the Lingang New Area) may entrust the consignee or other agents filed with the Chinese Customs to submit applications to the Shanghai Customs for pre-determination of classification of goods or price and place of origin in accordance with the relevant provisions of the Provisional Measures for Pre-determination Administration and the Announcement of the General Administration of Customs No. 14 of 2018 (Announcement of Matters Relating to the Implementation of the Shanghai Customs issued the Decision on Pre-determination after passing the examination in accordance with the Interim Measures for the Administration of Pre-determination and Announcement No. 14.

(b) The validity period, retroactivity, cancellation, information disclosure and other matters of the Decision on Advance Ruling made on the application of overseas exporters or producers shall be implemented in accordance with the Interim Measures for the Administration of Advance Rulings and Circular No. 14.

(c) If the consignee is not an applicant for an Advance Ruling Decision made on the application of an overseas exporter or producer, it cannot use the Advance Ruling Decision when importing the relevant goods. If necessary, the consignee shall apply to the Customs for an advance ruling in accordance with the Interim Measures for the Administration of Advance Rulings and Circular No. 14.

Specific implementation matters will be announced separately by Shanghai Customs.

III. Revision of the content of the form of the Pre-Determination Decision

In order to standardise the content of the relevant instruments and to safeguard the legitimate rights and interests of applicants, the format and content of the Pre-determination Decision in Annex 5 of Circular No. 14 have been amended (see annex).

This announcement shall come into effect on 1 May 2024. Where there is any inconsistency between the relevant matters in this Notice and Notice 14, this Notice shall prevail.

LINK

http://www.customs.gov.cn/customs/302249/302266/302267/5769044/index.html

Policy Interpretation:

Recently, the General Administration of Customs issued an announcement on the implementation of the Customs Advance Ruling Extension and other related matters, which further clarifies the requirements related to the advance ruling work, the main contents are as follows:

I. Implementation of customs advance ruling extension

Article 13 of the Interim Measures of the Peoples Republic of China for the Administration of Customs Advance Rulings (issued by Decree No. 236 of the General Administration of Customs and amended by Decree No. 262 of the General Administration of Customs, hereinafter referred to as the Interim Measures) stipulates that "Advance Ruling Decision shall be valid for a period of three years". This Supplementary Notice further clarifies that before the expiry of the validity period of the "Decision on Advance Ruling of the Customs of the Peoples Republic of China (Commodity Classification, Price and Origin)" (hereinafter referred to as the "Decision on Advance Ruling"), the original applicant may apply for an extension of the Decision on Advance Ruling from the customs.

Extension applications are subject to the following conditions:

(i) The applicant shall have 30 to 90 days (natural days, hereinafter the same) before the expiry date of the Preliminary Ruling Decision.

Example: The validity period of the Preliminary Decision ends on 30 October 2023, and the original applicant submitted an application for extension on 15 July 2023, which was more than 90 days from the expiry date of the validity period, so it did not meet the requirements for the timing of the application and could not apply for an extension.

The Pre-Determination Decision is valid until 30 October 2023, and the original applicant filed an application for extension on 15 September 2023, which meets the requirements of the time limit for filing an application for extension.

(ii) The customs matters and commodities involved in the Preliminary Ruling Decision for which an extension is requested shall remain unchanged.

Example: The merchandise covered by the Advance Ruling Decision for which a renewal application is made has been upgraded and modernised, with no change in the name of the merchandise, but with differences in its structure and function. Since the relevant commodity information involved in the application for extension is different from that in the original "Advance Ruling Decision (Commodity Classification)", it is not possible to apply for extension. If necessary, the applicant should submit an Application for Advance Ruling by the Customs of the Peoples Republic of China.

(iii) Customs will not accept applications for extension in the following four cases:

1. Where the Pre-Determination Decision has lapsed or been cancelled;

2. Changes in the applicants name, enterprise code and unified social credit code;

3. Failure to submit the application within the prescribed period;

4. After the issuance of the Advance Ruling Decision, the relevant customs regulations and announcements of the General Administration of Customs have made clear provisions on customs matters such as the classification of goods, prices and places of origin involved in the Advance Ruling Decision.

Except for special circumstances, the Customs shall complete the examination and approval within 30 days from the date of receipt of the applicants application for extension of the Decision on Advance Ruling. If the examination is passed, the Customs shall issue a new Preliminary Ruling Decision, and the relevant operation system shall correspondingly generate a new Preliminary Ruling Decision number, and the original Preliminary Ruling Decision shall automatically become invalid. If, upon examination and approval, it is found that there are circumstances listed in the foregoing that do not accept the application for renewal, the Customs shall return the relevant application with reasons and shall not renew it.

II. Expanding the range of applicants for advance rulings

Article 4 of the Interim Measures specifies that the applicant for advance ruling is "a foreign trade operator who is related to actual import and export activities and who has filed a record with the Customs", and this announcement specifies that overseas exporters or producers are permitted to apply for advance ruling on a pilot basis in the China (Shanghai) Pilot Free Trade Zone (including the Lingang New Area). This is another innovative initiative of the Customs to continuously optimise the business environment and promote trade facilitation and security in line with the international high-standard economic and trade rules.

There are three conditions that should be met for an overseas exporter or producer to apply for a customs advance ruling:

Firstly, it has signed a contract of sale of goods with the consignee of imported goods in China (Shanghai) Pilot Free Trade Zone and Lingang New Area; secondly, it should entrust the consignee or other agent who has filed an application with China Customs; thirdly, it should submit an application to Shanghai Customs.

It should be noted that, according to article 15 of the Interim Measures, "An applicant who imports or exports goods under the same circumstances as those set out in the Advance Ruling Decision within the validity period of the Advance Ruling Decision shall make a declaration in accordance with the Advance Ruling Decision, and the Customs Service shall give its approval". As for the pre-determination applied by the overseas applicant, the consignee of the imported goods is not the applicant of the pre-determination, and the Pre-determination Decision cannot be used when importing the relevant goods. If the consignee needs it, it should apply to the Customs for a pre-determination in accordance with the Interim Measures for the Administration of Pre-determination and the General Administration of Customs Announcement No. 14 of 2018.

III. Revision of the format of the Pre-Determination Decision

In accordance with the above revisions, the format of the Pre-determination Decision Letter was changed accordingly, with the addition of the basis for making the pre-determination and the means of relief, and the dedicated mailbox for administrative reconsideration.

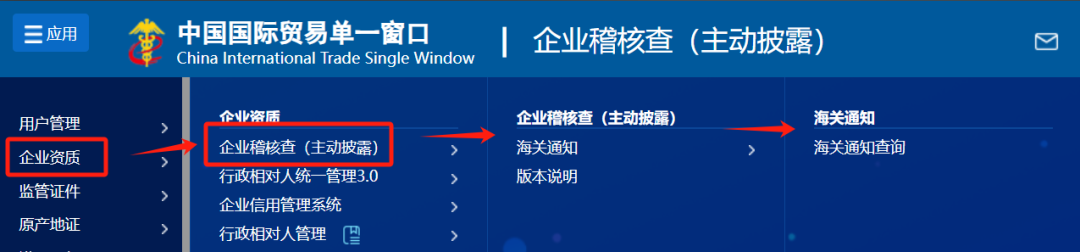

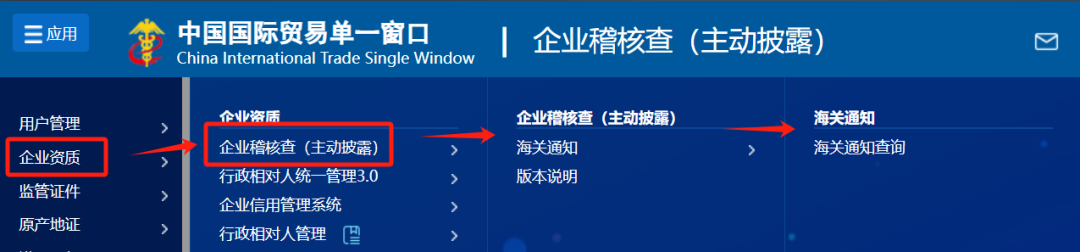

3.General Administration of Customs Announcement No. 36 of 2024 (Announcement on the "China International Trade Single Window" on-line "Enterprise Audit Check (Proactive Disclosure)" Functional Module)

Issuance Date: 2024-04-06

Effective Date: 2024-04-06

In order to further enhance the level of cross-border trade facilitation and continuously optimise the business environment at ports, the General Administration of Customs has put on-line the functional module of "Enterprise Audit Check (Proactive Disclosure)" under the item of "Enterprise Management" in the "China International Trade Single Window" (website: https://www.singlewindow.cn). Under the "Enterprise Audit Check (Active Disclosure)" function module, enterprises can sign and receive documents, submit applications for active disclosure and related materials through this function module, and receive feedback from the Customs on the handling of the situation.

LINK

http://www.customs.gov.cn/customs/302249/302266/302267/5797279/index.html

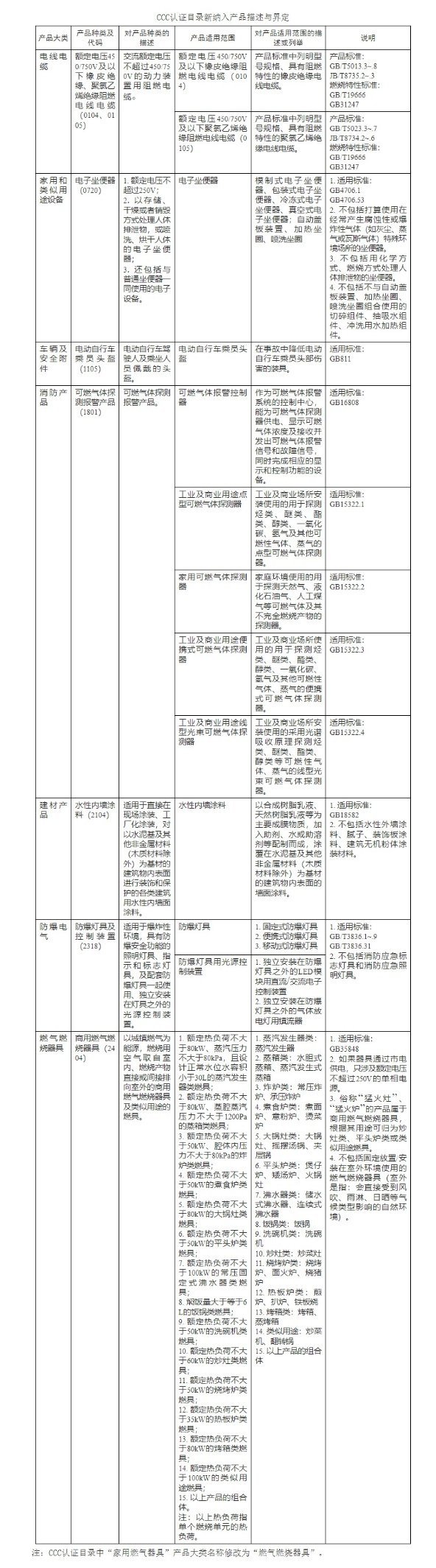

4.General Administration of Market Supervision on the commercial gas burners and other products to implement mandatory product certification management announcement

Issuance Date: 2024-03-21

Effective Date: 2024-04-07

In order to further strengthen product quality and safety supervision, according to the "Certification and Accreditation Regulations of the Peoples Republic of China," the relevant provisions of the General Administration of Market Supervision has decided to implement mandatory product certification of commercial gas burning appliances and other products (hereinafter referred to as CCC certification) management of low-voltage components to restore the third-party evaluation of CCC certification. The relevant requirements are announced as follows:

First, the commercial gas burners, flame retardant wires and cables, electronic toilets, electric bicycle helmets, combustible gas detection and alarm products, water-based interior paints, explosion-proof lighting and control devices to implement the management of CCC certification (see the annex for details of the description and definition of the product).

(a) From 1 May 2025, electric bicycle passenger helmets, explosion-proof lamps and control devices included in the CCC certification catalogue shall be certified by CCC and marked with the CCC certification mark before they are allowed to be shipped, sold, imported or used in other business activities.

May 1, 2024 onwards, the designated certification body began to accept CCC certification commission, involving the certification and testing work respectively by the current motorbike crew helmets, explosion-proof electrical designated business scope of certification bodies and laboratories to undertake.

(b) July 1, 2025 onwards, included in the CCC certification directory of commercial gas-burning appliances, flame-retardant wires and cables, electronic toilets, combustible gas detection and alarm products, water-based interior paints, should be certified by the CCC and marked with the CCC certification mark before leaving the factory, sales, imports, or used in other business activities.

July 1, 2024 onwards, the designated certification body to start accepting CCC certification entrusted to the certification work involved by the certification body now has the corresponding product category designated scope of business to undertake, the laboratory will be separately designated.

Secondly, the third-party evaluation method of CCC certification is resumed for low-voltage components.

(a) From 1 November 2024, low-voltage components should obtain CCC certification and marked with the CCC certification mark before they can be shipped, sold, imported or used in other business activities.

May 1, 2024 onwards, the designated certification body to start accepting low-voltage components CCC certification entrusted to the "mandatory certification of product conformity self-declaration of information reporting system" (hereinafter referred to as the system) is no longer generated self-declaration. For low-voltage components with a valid CCC self-declaration, the designated certification body to directly replace the CCC certificate, through the post-certification supervision to ensure the validity of the certification.

November 1, 2024, holding a valid CCC self-declaration of the enterprise should complete the conversion of CCC certification, and timely cancellation of the corresponding self-declaration; for the factory and no longer continue to produce, no need to convert. 2024 November 1, the system of low-voltage components in the CCC self-declaration will be uniformly cancelled.

(b) Restore the "General Administration of Market Supervision on adjusting and improving the mandatory product certification directory and implementation requirements of the announcement" (No. 44 of 2019) cancellation of the four certification bodies (China Quality Certification Centre, Fangyuan Logo Certification Group Co., Ltd., Guangdong Quality Supervision, Inspection and Certification Co. The testing work is still undertaken by the existing low-voltage components CCC certification designated laboratory.

Third, the designated certification body shall be based on the CCC certification of general rules and the corresponding product CCC certification and implementation rules for the development of certification and implementation details, and to the General Administration of Market Supervision Certification and Supervision Division for the record, before carrying out certification work.

Fourth, the designated certification bodies and laboratories should be certified under the premise of controllable risk, to ensure the quality of certification, and actively adopt the results of the existing conformity assessment, to reduce the burden on enterprises, to facilitate the certification of enterprises.

LINK

https://www.samr.gov.cn/zw/zfxxgk/fdzdgknr/rzjgs/art/2024/art_173693fdaf6e431fa242886c7a953631.html

5.Ministry of Commerce Ministry of Ecology and Environment General Administration of Customs Announcement No. 7 of 2024 "Announcement on the Release of the Third Catalogue of Products for Maintenance in Comprehensive Bonded Zones

Issuance Date: 2024-02-29

Effective Date: 2024-02-29

In order to support the enterprises in the comprehensive bonded zone to carry out high-tech, high value-added, environmentally friendly maintenance business, according to the "Opinions of the General Office of the State Council on Accelerating the Development of New Forms and Modes of Foreign Trade" (Guo Ban Fa [[]2021] No. 24), "Opinions of the General Office of the State Council on Promoting the Maintenance of Stability and Improvement of Quality of Foreign Trade" (Guo Ban Fa [[]2022] No. 18), "The Opinions of the Ministry of Commerce and Other 10 Departments on Enhancing the Opinions of the Ministry of Commerce and Other 10 Departments on Enhancing the Development Level of Processing Trade (Commerce and Trade Development [[]2023] No. 308) and other documents, the relevant matters are announced as follows:

I. Enterprises in the Comprehensive Free Trade Zone (hereinafter referred to as enterprises in the zone) may carry out maintenance business for aircraft engine nacelles, automobile transmissions, projectors and other products (see the annex for the catalogue).

II. Enterprises in the zone are allowed to carry out bonded repair business for self-produced products sold domestically by the Group and return to the country after repair, without the restriction of repair product catalogue.

III. Allow domestic goods to be repaired and belonging to the catalogue of goods to be repaired in the comprehensive bonded zone to be repaired in the comprehensive bonded zone and then directly exported to foreign countries.

IV. The Administrative Committee of the Comprehensive Free Trade Zone (or the local government administrative agency assigned to it) shall effectively carry out the main responsibility, regularly organise the bonded maintenance business in the zone to carry out the assessment of safety production, environmental protection, customs supervision, etc., and carry out rectification and other treatments for the non-compliant enterprises in accordance with the regulations. During the period of rectification, the enterprises shall not carry out bonded maintenance business, and after completing the rectification and reporting the rectification results to the Administrative Committee of the Comprehensive Free Trade Zone (or the local government administrative agency assigned to it) for approval, the enterprises can only carry out new bonded maintenance business.

V. Other matters involving maintenance business are still implemented in accordance with the Announcement No. 16 of 2020 of the Ministry of Commerce, Ministry of Ecology and Environment and General Administration of Customs "Announcement on Supporting Enterprises to Carry out Maintenance Business in Comprehensive Bonded Zones" and the Announcement No. 45 of 2021 of the Ministry of Commerce, Ministry of Ecology and Environment and General Administration of Customs "Announcement on the Issuance of Additional Catalogue of Maintenance Products in Comprehensive Bonded Zones" and so on. If the relevant contents of the above announcements are inconsistent with this announcement, this announcement shall prevail.

VI. The present bulletin shall enter into force on the date of its issuance.

LINK

http://www.mofcom.gov.cn/article/zcfb/zcblgg/202403/20240303480741.shtml

Policy Interpretation:

On 29 February 2024, the Announcement on the Release of the Third Batch of Maintenance Catalogue of the Comprehensive Bonded Zone (Ministry of Commerce, Ministry of Ecology and Environment, General Administration of Customs Announcement No. 7 of 2024) came into force, and the new catalogue includes 27 types of products such as aircraft engine nacelles, automobile gearboxes, projectors, and so forth, and the number of products that can be carried out as bonded maintenance products within the Comprehensive Bonded Zone has thus increased to 97 types. At the same time, the announcement made it clear that the enterprises in the zone are allowed to carry out the maintenance of self-produced products sold in the groups domestic sales, and return to the country after maintenance without the restriction of the maintenance catalogue; it is also allowed that the goods to be repaired domestically and belong to the goods in the maintenance catalogue are exported directly to the outside of the country after entering into the Comprehensive Bonded Zone for maintenance. The new regulations further release the bonded maintenance policy dividends of the zone, promote the development of new modes of foreign trade, and help enterprises reduce costs and increase efficiency.

6.Pharmacovigilance comprehensive equipment management [[]2024] No. 32 State Drug Administration Comprehensive Department on the issuance of 2024 national medical device sampling product testing programme notice

Issuance Date: 2024-03-19

Effective Date: 2024-03-19

Provinces, autonomous regions, municipalities directly under the Central Government and Xinjiang Production and Construction Corps and Drug Administration, the China Food and Drug Administration Research Institute, the relevant inspection agency:

According to the Notice of the Comprehensive Department of the State Drug Administration on Carrying out the National Medical Device Quality Sampling and Inspection Work in 2024 (Drug Supervision and General Mechanical Control [[]2024] No. 14), the National Medical Device Sampling and Inspection Product Inspection Programme for 2024 is hereby issued to you, and please organise and implement it conscientiously and put forward the following requirements:

I. Requirements for inspection work

Provinces, autonomous regions, municipalities directly under the Central Government and Xinjiang Production and Construction Corps and Drug Administration, China Food and Drug Certification and Research Institute should be in accordance with the 2024 national medical device sampling varieties of inspection programme (see Annex 1), the organization of the relevant inspection agency in accordance with the mandatory standards for medical devices, registered or filed product technical requirements to carry out the inspection work.

Inspection agencies should strengthen the test programme in accordance with the failure to complete all applicable projects to test the collection of the situation. For the registrant filer or imported products agent failed to provide all the information required to complete the test and supporting necessities, as well as product technical requirements are not perfect, resulting in the inability to complete the test, should be filed to the registrant or imported products agent of the provincial drug supervision and management department issued by the national medical device sampling missing test prompt letter, the prompt will be passed through the National Medical Device Sampling Information System, the prompt. The provincial drug supervision and management department shall investigate and deal with the relevant situation in a timely manner. For no valid reason does not cooperate with the quality of medical devices sampling inspection work, the results of the investigation should be recorded in the corporate credit file, and through other forms of strengthening the supervision and management of enterprises and related products, increase the intensity and frequency of supervision and inspection. For the product technical requirements are not perfect, should supervise the enterprise as soon as possible to improve the product technical requirements, and in accordance with the law to complete the change. The results of the relevant investigation and treatment should be entered into the national medical device sampling information system within 30 working days after the issuance of the reminder letter.

II. Requirements for the review process

2024 national supervision and sampling re-inspection acceptance department for medical devices registrant filer or imported products agent location of the provincial drug supervision and management department. The application for re-inspection of the same test report will be processed only once. Acceptance of re-inspection application of the provincial drug supervision and management department based on the 2024 national medical device sampling inspection re-inspection agency list (see Annex 2), to determine the re-inspection agency for re-inspection, re-inspection agency shall not be refused. No re-inspection will be carried out for the inspection programme which is explicitly for risk monitoring sampling.

Included in the list of re-inspection organisations, inspection bodies should continue to maintain their corresponding varieties and items of inspection capacity, inspection qualifications, the obligation to undertake provincial sampling and local drug supervision and management departments in the enforcement of re-inspection work. The re-inspection organisations should take the initiative to disclose the contact information of the re-inspection, and provide convenience for the re-inspection work. 2024 National Medical Device Sampling and Re-inspection Work Requirements are detailed in Annex 3.

The parties have objections to the test conclusions and can not be verified by re-inspection, you can submit a written application to the local provincial drug supervision and management department to object to the complaint, the specific time limit and process in accordance with the "National Medical Device Quality Sampling and Inspection Procedures" (drug supervision and comprehensive mechanical management [[]2021] No. 46) in the relevant objections to the complaint provisions for processing.

III. Requirements for the disposal of test results

The medical device registrant filer and sampled units should take risk control measures immediately after receiving the report of product non-compliance. Drug supervision and management departments should promptly organise investigation and disposal, meet the conditions for filing, timely filing and investigation; suspected of committing a crime, transferred to the judicial authorities according to law.

LINK

https://www.nmpa.gov.cn/xxgk/fgwj/gzwj/gzwjylqx/20240319094748118.html

7.MOFCOM Announcement No. 8 of 2024 Announcement of the Final Review Ruling on Anti-Dumping Measures Applied to Imports of Methyl Isobutyl (Methyl) Ketone Originating in the Republic of Korea, Japan and South Africa

Issuance Date: 2024-03-19

Effective Date: 2024-03-20

On 19 March 2018, the Ministry of Commerce (MOFCOM) issued Announcement No. 27 of 2018, deciding to impose anti-dumping duties on imports of methyl isobutyl (methyl) ketone originating from South Korea, Japan and South Africa from 20 March 2018 onwards, with an implementation period of five years. Among them, the duty rates are 18.5 per cent-32.3 per cent for South Korean companies, 45.0 per cent-190.4 per cent for Japanese companies, and 15.9 per cent-34.1 per cent for South African companies.

On 19 March 2023, upon the application of the Chinese methyl isobutyl (methyl) ketone industry, the Ministry of Commerce (MOFCOM) issued Announcement No. 9 of 2023, deciding to conduct a final review investigation from 20 March 2023 on the anti-dumping measures applied to imports of methyl isobutyl (methyl) ketone originating from the Republic of Korea, Japan and South Africa.

The Ministry of Commerce ("MOFCOM") investigated the likelihood of continuation or recurrence of dumping of imported methyl isobutyl (methyl) ketone ("MIC") originating from the Republic of Korea, Japan, and South Africa, and the likelihood of continuation or recurrence of injury to Chinas MIC industry if the anti-dumping measures were terminated, and issued a decision on review pursuant to Article 48 of the Regulations of the Peoples Republic of China on Antidumping ("Anti-Dumping Regulations") ( See Annex). The relevant matters are announced as follows:

I. Review of decisions

MOFCOM ruled that if the anti-dumping measures were terminated, dumping of imported methyl isobutyl (methyl) ketone originating from Korea, Japan and South Africa into China could continue or recur, and that the damage caused to Chinas methyl isobutyl (methyl) ketone industry could continue or recur.

II. Anti-dumping measures

In accordance with the provisions of Article 50 of the Anti-Dumping Regulations, the Ministry of Commerce, on the basis of the investigation results, proposed to the Customs Tariff Commission of the State Council to continue to implement anti-dumping measures, and the Customs Tariff Commission of the State Council, on the basis of the proposal of the Ministry of Commerce, made a decision that, with effect from 20 March 2024, anti-dumping duties would continue to be levied on the imports of Methyl Isobutyl (Methyl) Ketone originating from the Republic of Korea, Japan and South Africa, for an implementation period of five years.

The scope of products on which anti-dumping duties are levied are those to which the original anti-dumping measures apply, consistent with the scope of products in MOFCOM Announcement No. 27 of 2018. The details are as follows:

Name of product investigated: Methyl isobutyl (methyl) ketone.

Chemical name: 4-methyl-2-pentanone

English name: Methyl Isobutyl Ketone; 4-Methyl-2-Pentanone

Chemical molecular formula: C H O612

Chemical structural formula:

CH3 O

| ‖

CH3-CH-CH2-C-CH3

Product description: Methyl isobutyl (methyl) ketone is a colourless transparent flammable liquid with camphor-like odour. Slightly soluble in water, miscible with phenol, ether, aldehyde and other organic solvents, animal and vegetable oil, mineral oil.

Main uses: Methyl isobutyl (methyl) ketone is an excellent mid-boiling point solvent and organic synthesis raw materials, a wide range of uses. In terms of solvent, it is mainly used in paint, medicine, pesticide, solvent dewaxing solvent, rare metal extractant, magnetic tape, ink, epoxy resin, adhesive, atomic absorption photometric analysis, etc. It can also be used as a solvent for the production of automobile high-grade paint, ship paint, container paint, etc. In terms of organic synthetic raw materials, Methyl Isobutyl (Methyl) Ketone is the raw material for the synthesis of rubber antioxidant 4020, Methyl Isobutyl Methyl Alcohol, polymer initiator, epoxy resin latent curing agent, special surfactant and so on. In organic synthesis raw materials, methyl isobutyl (methyl) ketone is the raw material of synthetic rubber antioxidant 4020, methyl isobutyl methanol, polymer initiator, epoxy resin latent curing agent, special surfactants, etc.

This product is classified under the Import and Export Tariff of the Peoples Republic of China: 29141300.

The rates of anti-dumping duties continued to be levied are the same as those stipulated in the Ministry of Commerces Announcement No. 27 of 2018. The anti-dumping duty rates imposed on the companies are as follows:

Korean company.

1. Kumho P&B Chemical Co. 18.5 per cent

(kumho p&b chemicals, inc.)

2. Other Korean companies 32.3 per cent

Japanese companies:

1. Mitsui Chemicals Co., Ltd. 45.0 per cent

(Mitsui Chemicals, Inc.)

2. Mitsubishi Chemical Corporation 47.8%

(Mitsubishi Chemical Corporation)

3. Other Japanese companies 190.4 per cent

South African companies:

1. Sasol South Africa Limited 15.9 per cent

(Sasol South Africa Ltd)

2. Other South African companies 34.1%

III. Methodology for the imposition of anti-dumping duties

From 20 March 2024 onwards, import operators shall pay the corresponding anti-dumping duty to the Customs of the Peoples Republic of China when importing methyl isobutyl (methyl) ketone originating from the Republic of Korea, Japan and South Africa. The anti-dumping duty shall be levied ad valorem on the duty-paid price audited by the Customs, and the formula is: anti-dumping duty amount = customs duty-paid price × anti-dumping duty rate. Import VAT is levied ad valorem on the customs-validated duty-paid price plus customs duty and anti-dumping duty as the taxable price.

IV. Administrative review and administrative litigation

According to Article 53 of the Anti-Dumping Regulations, those who are not satisfied with the decision of this review may apply for administrative reconsideration in accordance with the law, or file a lawsuit with the Peoples Court in accordance with the law.

V. Implementation of the present bulletin as from 20 March 2024

LINK

http://www.mofcom.gov.cn/article/zcfb/zcblgg/202403/20240303482386.shtml

8.MOFCOM Announcement No. 9 of 2024 Announcement on the Initiation of End-of-Term Review Investigation on Anti-Dumping Measures Applied to Imports of Resorcinol Originating in Japan

Issuance Date: 2024-03-22

Effective Date: 2024-03-22

On 22 March 2013, the Ministry of Commerce ("MOFCOM") issued Announcement No. 13 of 2013, deciding to impose anti-dumping duties on imports of resorcinol originating from Japan and the United States at the rates of 40.5% for Japan and 30.1% for the U.S. Effective from 23 March 2013, the Ministry of Commerce ("MOFCOM") issued Announcement No. 10 of 2019, deciding to impose anti-dumping duties on imports of resorcinol to continue to impose anti-dumping duties for an implementation period of five years.

On 2 January 2024, the Ministry of Commerce (MOFCOM) received an application for final review of anti-dumping measures from Zhejiang Hongsheng Chemical Co., Ltd. on behalf of the domestic resorcinol industry. The applicant claimed that if the anti-dumping measures were terminated, the dumping of imported resorcinol originating from Japan on China might continue or reoccur, and the damage caused to the Chinese industry might continue or reoccur, and requested MOFCOM to conduct a final review investigation of the imported resorcinol originating from Japan, and to maintain the anti-dumping measures imposed on the imported resorcinol originating from Japan. The petitioner did not file an application for final review of the anti-dumping measures applied to the imports of resorcinol originating in the United States.

In accordance with the relevant provisions of the Regulations of the Peoples Republic of China on Anti-Dumping, the Ministry of Commerce (MOFCOM) examined the applicants qualifications, the situation of the investigated products and similar products in China, the import situation of the investigated products during the period of the implementation of the anti-dumping measures, the possibility of the continuation or reoccurrence of dumping, the possibility of the continuation or reoccurrence of damage, and the relevant evidence. The available evidence shows that the applicant meets the requirements of Articles 11, 13 and 17 of the Anti-Dumping Regulations of the Peoples Republic of China regarding the industry and its representation, and that it is qualified to file the application on behalf of the Chinese resorcinol industry. The investigating authority concluded that the applicants claims and the prima facie evidence submitted met the requirements for filing a final review case.

In accordance with Article 48 of the Anti-Dumping Regulations of the Peoples Republic of China, the Ministry of Commerce (MOFCOM) has decided to conduct an end-of-period review (EPR) investigation from 23 March 2024 on the anti-dumping measures applied to the imports of resorcinol originating from Japan. The relevant matters are announced as follows:

I. Continuation of anti-dumping measures

Based on the recommendation of the Ministry of Commerce, the Customs Tariff Commission of the State Council decided to continue to impose anti-dumping duties on the imported resorcinol originating from Japan in accordance with the scope of the levied products and the duty rate published in the Announcement No. 10 of 2019 of the Ministry of Commerce during the period of the end-of-period review investigation of the anti-dumping measures. From 23 March 2024, the anti-dumping measures applicable to the imports of resorcinol originating in the United States expired and were terminated.

The anti-dumping duty rates imposed on the companies are as follows:

1. Sumitomo Chemical Co., Ltd. 40.5 per cent

(Sumitomo Chemical Company, Limited)

2. Mitsui Chemicals Co., Ltd. 40.5 per cent

(Mitsui Chemicals, Inc.)

3. Other Japanese companies 40.5 per cent

II. Review of the investigation period

The dumping investigation period for this review is from 1 January 2023 to 31 December 2023, and the industrial injury investigation period is from 1 January 2019 to 31 December 2023.

III. Scope of products for review investigations

The scope of products under review are those to which the original anti-dumping measures applied, and are consistent with the scope of products to which the anti-dumping measures applied as announced in the Ministry of Commerces Announcement No. 10 of 2019, as follows.

Name of product investigated: resorcinol, also known as 1,3-benzenediol and resorcin.

English name: M-dihydroxybenzene or Resorcinol.

Molecular formula: C6H6O2

Chemical structural formula:

Physical and Chemical Characteristics: usually white needle-like crystals, will gradually turn red when exposed to air, easily soluble in water, ethanol, ether, soluble in chloroform, carbon tetrachloride, insoluble in benzene.

Main uses: Resorcinol is an important chemical synthesis intermediate and fine chemical material, mainly used in the production of rubber adhesives and ultraviolet absorbers. In addition, resorcinol can also be used in the production of wood adhesives, flame retardants and a variety of pharmaceutical and pesticide intermediates.

This product is classified under the Import and Export Tariff Code of the Peoples Republic of China: 29072100.Resorcinol salts under this tariff code are not included in the scope of the products under investigation.

IV. Content of the review

This review investigation is about whether the termination of anti-dumping measures on imports of resorcinol originating in Japan is likely to result in the continuation or recurrence of dumping and injury.

V. Registration for the survey

Stakeholders may register with the Trade Remedy Bureau of the Ministry of Commerce to participate in the anti-dumping final review investigation within 20 days from the date of publication of this announcement. Stakeholders participating in the investigation shall, according to the Reference Form for Registration for Participation in the Investigation, provide basic identification information, the quantity and amount of the products under investigation exported or imported to China, the quantity and amount of the production and sale of similar products, as well as explanatory materials such as the situation of association. The Reference Form for Registration for Participation in the Investigation can be downloaded from the sub-site of the Trade Remedy Investigation Bureau on the website of the Ministry of Commerce.

Stakeholders registering to participate in this anti-dumping investigation shall submit an electronic version through the Trade Remedy Investigation Informationisation Platform (https://etrb.mofcom.gov.cn) and a written version at the same time as required by the Ministry of Commerce. The content of the electronic version and the written version should be the same, and the format should be consistent.

The stakeholders referred to in this announcement are the individuals and organisations specified in Article 19 of the Anti-Dumping Regulations of the Peoples Republic of China.

VI. Access to public information

Interested parties may download the non-confidential text of the application submitted by the applicant in this case from the sub-site of the Trade Remedies Investigation Bureau on the website of the Ministry of Commerce, or go to the Trade Remedies Public Information Inspection Room of the Ministry of Commerce (telephone number: 0086-10-65197856) to find, read, copy and photocopy the non-confidential text of the application submitted by the applicant in this case. In the course of the investigation, interested parties may search for the public information of the case through the relevant websites or go to the Trade Remedy Public Information Inspection Room of the Ministry of Commerce to find, read, transcribe and copy the public information of the case.

VII. comments on filings

Stakeholders who wish to comment on the scope of the products under investigation and the eligibility of the applicant, the country under investigation and other related issues may submit their written comments to the Trade Remedies Bureau of the Ministry of Commerce within 20 days from the date of publication of this announcement.

VIII. Modalities of the investigation

According to Article 20 of the Regulations of the Peoples Republic of China on Anti-Dumping, the Ministry of Commerce may use questionnaires, sampling, hearings, on-site verification and other means to obtain information from relevant stakeholders and conduct investigations.

In order to obtain the information required for the investigation of this case, MOFCOM usually issues the questionnaire to stakeholders within 10 working days from the closing date of the registration for participation in the investigation as stipulated in this announcement. Stakeholders can download the questionnaire from the sub-site of the Trade Remedies Investigation Bureau on the MOFCOM website.

Stakeholders should submit complete and accurate responses within the specified time frame. Responses should include all information requested in the questionnaire.

IX. Submission and processing of information

Stakeholders submitting comments, replies, etc. in the course of the investigation shall submit the electronic version through the Trade Remedy Investigation Informatisation Platform (https://etrb.mofcom.gov.cn) and the written version at the same time in accordance with the requirements of the Ministry of Commerce. The contents of the electronic version and the written version should be the same, and the format should be consistent.

If the information submitted to the MOFCOM by a stakeholder needs to be kept confidential, the stakeholder may submit a request to the MOFCOM for confidential treatment of the relevant information, stating the reasons for the request. If MOFCOM grants the request, the stakeholder applying for confidentiality shall also provide a non-confidential summary of the confidential information. The non-confidential summary should contain sufficient meaningful information to enable other stakeholders to have a reasonable understanding of the confidential information. If a non-confidential summary cannot be provided, a reason should be given. If the information submitted by the stakeholder does not indicate that it is confidential, the Ministry of Commerce will consider the information to be public.

X. Consequences of non-cooperation

According to Article 21 of the Regulations of the Peoples Republic of China on Anti-Dumping, when the Ministry of Commerce conducts an investigation, the interested party shall faithfully reflect the situation and provide relevant information. If the interested party fails to reflect the situation truthfully and provide relevant information, or fails to provide the necessary information within a reasonable time, or seriously obstructs the investigation in other ways, MOFCOM may make a ruling based on the facts obtained and the best available information.

XI. Duration of the investigation

The survey commenced on 23 March 2024 and should be completed by 23 March 2025 (excluding this date).

XII. Contact information of the Ministry of Commerce

Address: 2 East Changan Street, Beijing, China

Postcode: 100731

Trade Remedy Investigation Bureau, Ministry of Commerce, Import Investigation Division 1

Tel: 0086-10-65198757, 65198435

Fax: 0086-10-65198172

Website: Sub-website of the Trade Remedy Investigation Bureau on the website of the Ministry of Commerce (trb.mofcom.gov.cn)

LINK

http://www.mofcom.gov.cn/article/zcfb/zcblgg/202403/20240303485049.shtml

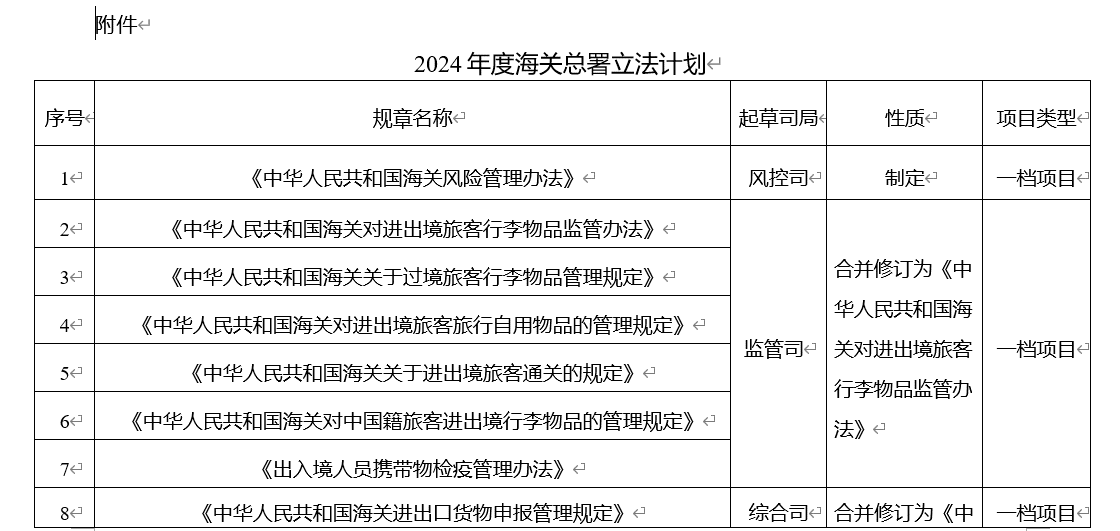

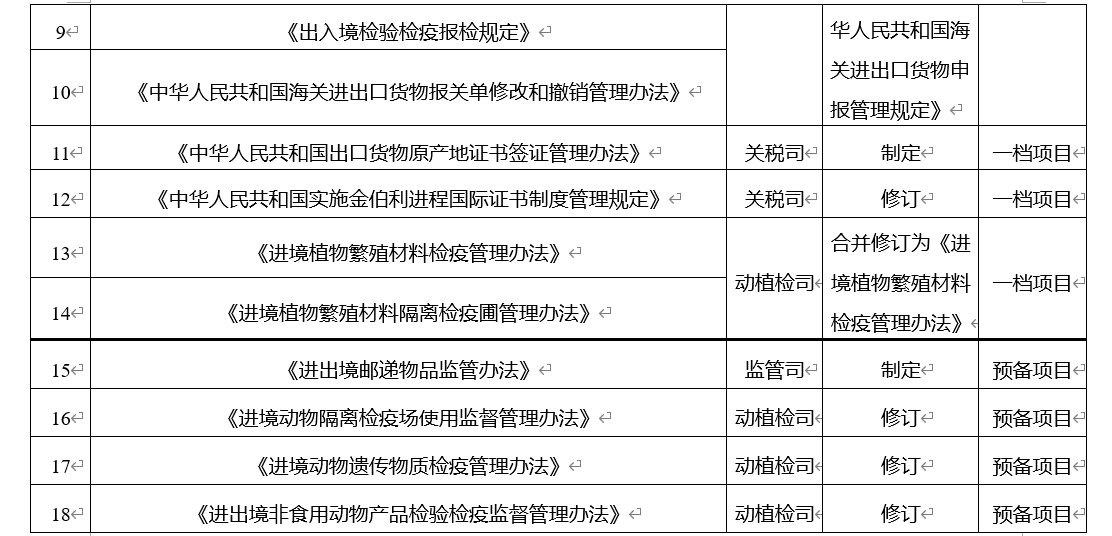

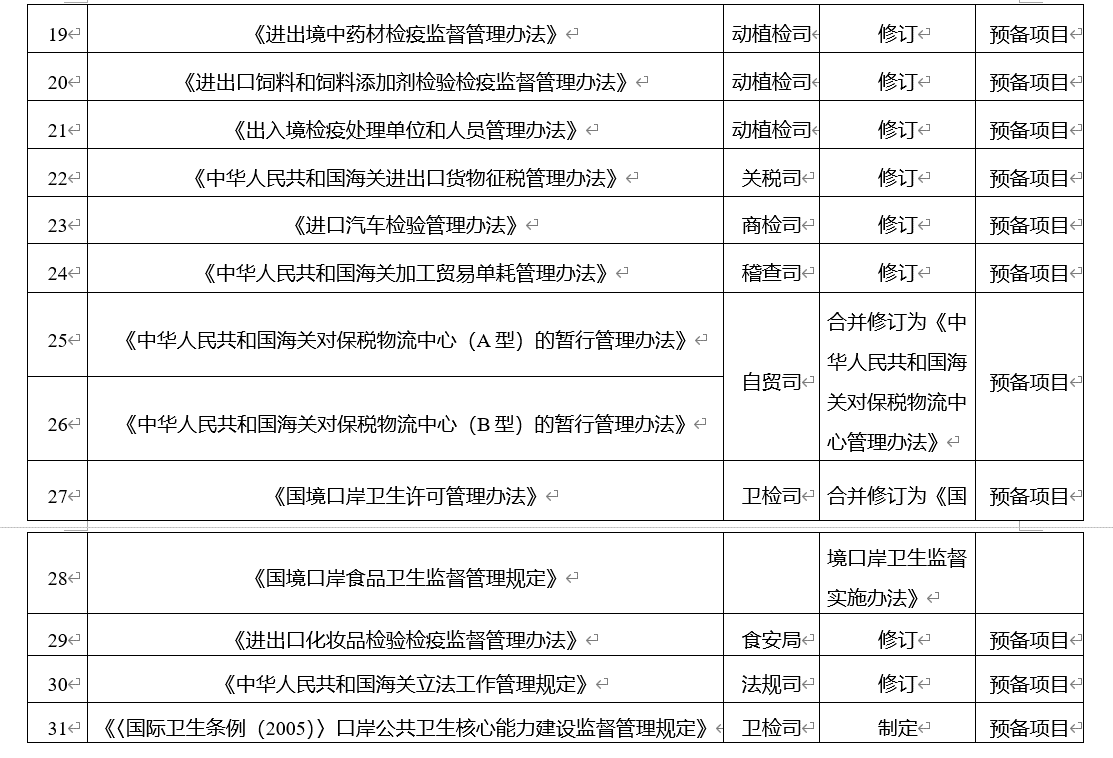

9.Department Law [[]2024] No. 33 Notice of the General Administration of Customs on the issuance of the Legislative Programme of the General Administration of Customs for the Year 2024

Issuance Date: 2024-03-22

Effective Date: 2024-03-22

The Legislative Plan of the General Administration of Customs for the Year 2024 (see annex) was considered and adopted by the General Administration of Customs at its meeting on 13 March 2024, and is hereby issued. All relevant departments are requested to implement the legislative plan in strict accordance with the legal procedures, further improve the system of customs laws and norms, and provide rule of law safeguards for the construction of modern customs.

LINK

http://www.customs.gov.cn/customs/302249/zfxxgk/zfxxgkml34/5774745/index.html

10.Department of Trade Letter [[]2024] No. 72 General Administration of Customs Ministry of Finance General Administration of Taxation State Administration of Foreign Exchange on the approval of the establishment of Ezhou Airport Bonded Logistics Centre (B-type) Letter

Issuance Date: 2024-03-15

Effective Date: 2024-03-15

Your companys "Application for Establishment of Bonded Logistics Centre (Type B)" has been received. According to the relevant regulations on the management of Bonded Logistics Centre (Type B), after examination and approval, it is agreed to set up Ezhou Airport Bonded Logistics Centre (Type B) (hereinafter referred to as Airport Bonded Logistics Centre), which will be responsible for the construction and operation by your company.

Airport Bonded Logistics Centre is located in the north side of Ezhou Huahu Airport, with a planning area of 0.1 square kilometres, and its four boundaries are as follows: east to the east runway of the airport, south to Huahu Airport, west to Aviation Boulevard, and north to Wuzhu Boulevard. Your company shall strictly follow the relevant requirements of Acceptance Standards for Bonded Logistics Centre Basic and Supervisory Facilities (issued by the Department of Gafa [[]2011] No. 426) to carry out the construction, and complete the relevant formalities such as land and construction planning in accordance with the law, and complete the construction and apply for acceptance within one year from the date of approval of the establishment of the bonded logistics centre. Upon completion of construction, Wuhan Customs, together with Hubei Supervision Bureau of the Ministry of Finance, Hubei Tax Bureau of the State Administration of Taxation and Hubei Sub-bureau of the State Administration of Foreign Exchange will conduct formal acceptance of the Airport Bonded Logistics Centre and report the results of the acceptance to the General Administration of Customs, the Ministry of Finance, the General Administration of Taxation and the State Administration of Foreign Exchange for review. The Airport Bonded Logistics Centre will be allowed to carry out relevant business only after the acceptance result has been approved.

The relevant tax policies of the Airport Bonded Logistics Centre are implemented in accordance with the relevant provisions of the Circular of the Ministry of Finance, the General Administration of Customs and the State Administration of Taxation on the Tax Policies Applicable during the Expansion of the Pilot Period of the Bonded Logistics Centre (Type B) (Cai Shui [[]2007] No. 125) and the Circular of the Ministry of Finance and the State Administration of Taxation on the Policies of Value-added Tax and Consumption Tax on Exported Goods and Services (Cai Shui [[]2012] No. 39); The foreign exchange policy is implemented in accordance with the relevant provisions of the Circular of the State Administration of Foreign Exchange on the Issuance of the Guidelines on Foreign Exchange Business for Current Accounts (2020 Edition) (Huifa [[]2020] No. 14).

Your company and the enterprises in the Airport Bonded Logistics Centre shall comply with the relevant national laws, administrative regulations and customs supervision and other relevant regulations, and bear the corresponding legal responsibilities. Please reflect any problems encountered in the process of construction and operation in a timely manner.

LINK

http://www.customs.gov.cn/customs/302249/zfxxgk/zfxxgkml34/5778158/index.html

11.State Market Supervision Competition Letter [[]2024] No. 40 Market Supervision Administration on the organisation to declare the third batch of national trade secret protection innovation pilot notice

Issuance Date: 2024-03-29

Effective Date: 2024-03-29

Market Supervision Bureaus (Offices and Commissions) of Provinces, Autonomous Regions, Municipalities directly under the Central Government and Xinjiang Production and Construction Corps:

In order to thoroughly implement the decision-making and deployment of the CPC Central Committee and the State Council on strengthening the protection of trade secrets, further enhance the level of protection of trade secrets in key areas around the national strategic planning layout, enhance the innovation capacity of key industries, maintain the security and stability of the industrial chain supply chain, and help develop new productivity, the General Administration of Market Supervision has decided to carry out the third batch of pilot work on the innovation of the protection of trade secrets in the country. The relevant matters are notified as follows:

I. Pilot subjects

The third batch of innovative pilot projects will be carried out in single-programme cities, sub-provincial cities, prefectural cities and municipal districts (counties) of municipalities directly under the Central Government, and applications will be submitted by the local peoples governments.

II. Working steps

(i) Pilot application. Local peoples governments, in accordance with the situation and development needs of trade secret protection in their regions, voluntarily submit applications for innovative pilot programmes, carefully prepare the application materials (see the annex for requirements) and submit them to the provincial market supervision departments.

(ii) Recommendation on merit. Provincial market supervision departments on the local submission of innovative pilot application materials for preliminary review, and then submit to the General Administration of Market Supervision on the basis of merit.

(iii) Evaluation and demonstration. The General Administration of Market Supervision organises experts to assess and validate the application materials of the innovation pilot, and selects 5-10 regions with a high degree of importance attached by the local government, a clear working idea, a clear direction of innovation, an outstanding advantage in key industries, and a better foundation for the work as the third batch of innovation pilot regions.

III. Work requirements

Provincial market supervision departments should attach great importance to the third batch of pilot work, and effectively do a good job in organising the declaration and initial examination and gatekeeping, and strengthen the tracking and guidance after the pilot list is determined. The market supervision departments of the application place should promptly report to the local party committee government for instructions, actively seek support, and effectively do a good job in the application of innovative pilot work.

Provincial market regulators are requested to submit the list of recommendations and application materials to the General Administration of Market Supervision (Price Supervision and Competition Bureau) before 30 April 2024 through the "Official Document Exchange System".

Contact: Price Supervision and Competition Bureau Zhang Guoning 010-82261263

LINK

https://www.samr.gov.cn/zw/zfxxgk/fdzdgknr/jjjzs/art/2024/art_154655288f2c405f895053cbba4eb3ca.html

12.Hui Fa [[]2024] No. 11 Circular of the State Administration of Foreign Exchange on Further Optimising the Management of Trade Foreign Exchange Businesses

Issuance Date: 2024-04-07

Effective Date: 2024-06-01

The branch offices of the State Administration of Foreign Exchange in all provinces, autonomous regions, municipalities directly under the central government and cities with separate plans, and all national Chinese banks:

In order to promote the high-quality development of trade and effectively enhance the ability to serve the real economy, the State Administration of Foreign Exchange (SAFE) has decided to further optimise the management of trade foreign exchange business and facilitate the handling of cross-border trade business by business entities. The relevant matters are notified as follows:

I. Optimising the registration and management of the "Directory of Trade Foreign Exchange Receipts and Payments Enterprises"

The requirement for approval by the State Administration of Foreign Exchange branches (hereinafter referred to as foreign exchange bureaux) for registration in the "Directory of Enterprises Receiving and Paying in Foreign Exchange for Trade" (hereinafter referred to as the Directory) has been cancelled, and the Directory will be registered by the banks in the country directly.

(a) Enterprises carrying out foreign exchange receipts and payments for trade in goods should register for the directory with domestic banks before making their first payment. When registering, they may submit the "Application Form for Directory of Enterprises Conducting Foreign Exchange Receipts and Expenditures of Trade in Goods" (hereinafter referred to as the "Application Form", see Annex 1) to the banks through online or offline means. The bank shall fill in the enterprise directory information through the bank side of the "Digital Foreign Exchange Control" platform of the State Administration of Foreign Exchange (hereinafter referred to as the "Digital Foreign Exchange Control" platform) in accordance with the Application Form, and inform the enterprise of the account number of the Internet side of the "Digital Foreign Exchange Control" platform and the account number of the Internet side of the "Digital Foreign Exchange Control" platform after completion of the filling. After the completion of filling in the information, the enterprise shall be informed of the account number and initial password of the Internet side of the "Digital Foreign Control" platform, and the enterprise can enquire about the results of the directory registration process through the Internet side of the "Digital Foreign Control" platform. Other domestic organisations or individual industrial and commercial households with objective needs to carry out foreign exchange receipts and payments business of trade in goods can refer to the relevant provisions for enterprises. Small and micro cross-border e-commerce enterprises are exempted from the aforementioned directory registration when they handle foreign exchange receipts and payments of trade in goods with the electronic information of transactions.

(b) In the event of a change in the name, unified social credit code, legal representative, contact information or registered address of an enterprise in the directory, the enterprise shall, within 30 days of the date of the change, apply for a change in the directory information at the domestic bank, either online or offline, on the basis of the explanatory materials setting out the change. If the bank discovers that the above information of the enterprise has been changed, it can take the initiative to change the directory information of the enterprise according to the internal approval process. If the foreign exchange bureau to which the enterprise belongs changes after the enterprise changes its place of registration, the enterprise shall report to the foreign exchange bureau in the original location. The cancellation of an enterprises directory shall be handled by the foreign exchange bureau in accordance with the regulations.

(c) Banks should review the authenticity of the basic information of enterprises and retain the paper or electronic materials for five years for inspection when they handle the business of filling in or changing the directory information.

Enterprises carrying out foreign exchange collection and payment business of trade in goods as referred to in this Article do not include payment institutions and banks providing agent settlement and sale of foreign exchange and related fund collection and payment services for cross-border trade in goods of the operating entities on the basis of the electronic information of the transactions; small and micro cross-border e-commerce enterprises refer to cross-border e-commerce enterprises with the cumulative amount of collection or payment of foreign exchange of trade in goods of less than the equivalent of 200,000 US dollars (excluded) in a year.

II. Simplification of procedures for trade receipts and payments by enterprises in special customs control areas

When an enterprise in a special customs supervision area handles foreign exchange receipts and expenditures for trade in goods, if the import and export unit is another organisation due to operational needs, the bank may, in accordance with the principle of exhibition, review the authenticity and reasonableness of the transaction as well as the relevant materials on the inconsistency between the subject of receiving and paying remittances and the subject of import and export and handle the transaction, and indicate "non-declarant" in the appendix of the declaration of the transaction of foreign exchange-related receipts and expenditures. ".

III. Relaxation of the exemption of trade in goods from the registration of special remittance authority

For Class A enterprises with a single transaction equivalent to less than USD 200,000 (inclusive), goods trade remittances with an interval of more than 180 days between the date of remittance and the original date of receipt or payment (not included), or goods trade remittances that cannot be returned in the original way due to special circumstances, can be handled by banks directly, except for those stipulated otherwise. When handling the above business for an enterprise, the bank shall confirm the authenticity and reasonableness of the overdue period or the inability to return the goods by the original route, and shall indicate "special remittance + type of remittance business (e.g., overdue period, non-original return)" in the addendum to the transaction of the declaration of foreign-related receipts and expenditures.

IV. Optimising the management of trade foreign exchange operations of enterprises in categories B and C

When Category B and C enterprises handle deferred collection or deferred payment business for more than 90 days (not included), if during the validity period of the classification and supervision, the situation that previously led to the inclusion of Category B and C enterprises has been improved or corrected, and there is no new situation of inclusion in the Category B and C enterprises, six months from the date of inclusion in the Category B and C enterprises, they can register at the local foreign exchange bureau, and the bank will handle this business for the enterprise with the "Registration Form for Trade Foreign Exchange Businesses" (see Appendix 2). ) for the enterprise to handle the business.

V. Clarification of the foreign exchange registration of trade in goods business processing materials

Integrate the relevant provisions of the Notice of the State Administration of Foreign Exchange on Issuing the Regulations on Foreign Exchange Management of Trade in Goods (Huifa [[]2012] No. 38) and the Notice of the State Administration of Foreign Exchange on Issuing the Guidelines on Foreign Exchange Business for Current Accounts (2020 Edition) (Huifa [[]2020] No. 14) on the foreign exchange registration business of trade in goods, and make clear the handling of the business related to the foreign exchange registration of trade in goods. Materials (see Annex 3).

VI. Revision of instruments relating to foreign exchange management of trade in goods

Simultaneous amendments to the "Notice of Classification Conclusion of XX Branch (Sub-branch) Bureau of the State Administration of Foreign Exchange", "Risk Alert Letter of XX Branch (Sub-branch) Bureau of the State Administration of Foreign Exchange" and "Verification Notification Letter of XX Branch (Sub-branch) Bureau of the State Administration of Foreign Exchange" annexed to the "Notice of the State Administration of Foreign Exchange on the Issuance of Guidelines on Foreign Exchange Business for Current Accounts (2020 Edition)" (Huifa [[]2020] No. 14) (see Annexes 4 - 6) .

This Circular shall come into effect on 1 June 2024, and the Circular of the State Administration of Foreign Exchange on Issuing Regulations on Foreign Exchange Management of Trade in Goods on Relevant Issues (Huifa [[]2012] No. 38) shall be repealed at the same time. Where the previous regulations are inconsistent with the contents of this Circular, this Circular shall prevail. Upon receipt of this Circular, all SAFE branches shall promptly forward it to the branch offices in the mainland (municipalities) under their jurisdiction, urban commercial banks, rural commercial banks, wholly foreign-owned banks, sino-foreign joint venture banks, branches of foreign banks, and rural co-operative financial institutions, and all national Chinese banks shall promptly forward it to their subordinate branches. If there are any problems in the implementation, please provide timely feedback to the local foreign exchange bureaus.

LINK

http://www.safe.gov.cn/safe/2024/0407/24204.html

Policy Interpretation:

In order to thoroughly implement the spirit of the Central Financial Work Conference, deepen the reform of foreign exchange management of trade in goods, and promote the high-quality development of foreign trade, the State Administration of Foreign Exchange has recently issued the Circular of the State Administration of Foreign Exchange on Further Optimising the Management of Trade in Foreign Exchange Businesses (Huifa 〔2024〕 No. 11, hereinafter referred to as the Circular) to optimise the foreign exchange business process, further promote the facilitation of cross-border trade, and effectively enhance the quality and efficiency of services to the real economy. The Circular is effective from 1 June 2024 onwards.

The Notice consists of six policy measures, including three main aspects: first, optimising the registration management of the foreign trade enterprise list. Trade foreign exchange receipts and expenditures enterprise directory" processing mode, approved by the foreign exchange bureau adjusted to the bank directly. The second is to facilitate the settlement of cross-border trade foreign exchange revenue and expenditure of enterprises. Simplify the procedures for trade receipts and payments of enterprises in special customs supervision areas. Relaxing the authority of banks to handle special remittance for trade in goods (non-original return or remittance time exceeding 180 days). Optimise the deferred collection and payment of foreign exchange for B and C type enterprises. Thirdly, clean up and integrate the foreign exchange management regulations on trade in goods. Some documents were repealed, provisions on foreign exchange registration of trade in goods were consolidated, and styles of some instruments were revised.

In the next step, the State Administration of Foreign Exchange will continue to thoroughly implement the decision-making and deployment of the CPC Central Committee and the State Council, adhere to the integration of high-quality development and high level of security, promote the construction of a new pattern of development, enhance the quality and effectiveness of foreign exchange services for the real economy, further optimise the business environment, and help promote stability and improve the quality of foreign trade.

13.[2024]No.15 Circular of the Comprehensive Department of the State Administration of Foreign Exchange on Updating the Classification of Merchant Category Codes for Domestic Bank Cards Used Abroad

Issuance Date: 2024-03-22

Effective Date: 2024-03-22

Branch Offices of the State Administration of Foreign Exchange in all provinces, autonomous regions, municipalities directly under the Central Government and municipalities with separate plans, UnionPay International Company Limited, Connect (Hangzhou) Technical Services Company Limited, Wanshi Netlink Information Technology (Beijing) Company Limited, and all national Chinese-funded commercial banks:

In order to facilitate cross-border transactions by individuals using domestic bank cards and to improve the management of foreign exchange business of bank cards, we hereby notify you of the following matters relating to the updating of the classification and management of the Merchant Category Code (MCC) for domestic bank cards used abroad:

I. The addition of 345 merchant category codes (see Annex), together with the Merchant Category Codes for Domestic Bank Cards Used Overseas annexed to the Circular of the State Administration of Foreign Exchange on Regulating the Management of Foreign Currency Cards of Banks (Huifa [[]2010] No. 53, hereinafter referred to as Circular No. 53), constitutes the currently valid catalogue of the classification of merchant category codes.

II. Domestic bank card clearing agencies and card-issuing financial institutions shall, in accordance with the provisions of Circular No. 53, strictly implement the classification and management of overseas transactions of domestic bank cards, set up their business systems in accordance with the current valid merchant category code classification catalogue, and shall not authorize or clear transactions other than those listed in the merchant category code classification catalogue. Among them, bank cards authorised to be issued by domestic bank card clearing institutions shall be uniformly set up by domestic bank card clearing institutions in their business systems; bank cards authorised to be issued by overseas bank card clearing institutions shall be set up by each domestic card-issuing financial institution in its business system.

III. Domestic bank card clearing organisations adjusting their own merchant category codes should report the situation in writing to SAFE 30 days before the adjustment takes effect. For overseas bank card clearing organisations to adjust their merchant category codes, Bank of China, Industrial and Commercial Bank of China and China Merchants Bank shall report in writing to SAFE 30 days before the adjustment takes effect. SAFE updates and releases the classification catalogue of merchant category codes for domestic bank cards used overseas based on the adjustment of the merchant category codes.

Adjustment of merchant category code as mentioned above refers to the addition or deactivation of a merchant category code, or a change in the definition of a merchant category code, etc.

IV. This Circular shall be implemented as of 1 May 2024. All domestic bank card clearing agencies and card-issuing financial institutions shall complete the adjustment of their own business systems in a timely manner in accordance with the requirements of this Circular.

Upon receipt of this notice, the branch offices of SAFE in all provinces, autonomous regions, municipalities directly under the central government and municipalities with separate plans should immediately forward it to the municipal branch offices in the mainland under their jurisdiction, urban commercial banks, rural commercial banks, wholly foreign-owned banks, sino-foreign joint venture banks, branches of foreign banks, rural co-operative financial institutions, and village and township banks. If you encounter any problems in the implementation, please provide timely feedback to the Balance of Payments Department of SAFE. Tel: 010-68402309, 68402593.

LINK

http://www.safe.gov.cn/safe/2024/0322/24135.html

14.NDRC Hi-Tech [[]2024] No. 351 Circular of the National Development and Reform Commission and Other Departments on the Requirements for the Formulation of the List of Integrated Circuit Enterprises or Projects and Software Enterprises Enjoying Preferential Tax Policies in 2024

Issuance Date: 2024-03-21

Effective Date: 2024-03-21

Development and Reform Commission, department in charge of industry and information technology, and department (bureau) of finance of all provinces, autonomous regions, municipalities directly under the central government and municipalities directly under the central government, and Xinjiang Production and Construction Corps, Guangdong Branch Office of the General Administration of Customs and all customs offices directly under the central government, and tax bureaus of all provinces, autonomous regions, municipalities directly under the central government and municipalities directly under the central government and municipalities directly under the central government in the plan of State Administration of Taxation: